We talk about investing a lot and what you should do or what the historic data says is likely to happen. But the rubber does eventually hit the road and real investments are made. So now that 2015 is over, how did the Fox family do with our portfolio? It only seems fair to ask.

Investment performance

From an investment performance perspective, 2015 was definitely a subpar year. If historic returns are about 6-8%, we were well below that, sadly even dipping into negative territory for a couple investments.

| Investment |

Portfolio weight (beginning of 2015) |

Portfolio weight (end of 2015) |

2015 return |

| US stock index |

33% |

43% |

0.3% |

| International stock index |

35% |

36% |

-4.4% |

| REIT index |

11% |

11% |

2.4% |

| Commodities |

8% |

5% |

-28.2% |

| Medtronic |

9% |

1% |

8.1% |

| Bonds/Cash |

4% |

4% |

0.4% |

| TOTAL | -3% |

As you can see, pretty much all our investments were either flat or fell in value. Luckily, Medtronic had another good year, but even that wasn’t enough to compensate for the losers.

If you put it all in the pot and mix it up, our portfolio had a return of about -3%. Obviously that isn’t what we want, and returns like that aren’t going to make the Fox family secure in its retirement and other financial goals. But it’s important to keep in mind 2015 was the first down year since the disastrous year which was 2008. That was a 6-year winning streak, so it’s probably reasonable to expect that to end. Fortunately, if you were going to have a down year, this one was pretty benign as those things go.

Changes in investment weightings

If you read this column regularly, you know that in 2015 we had two major life changes that had a big impact on our finances. First, I quit my job at Medtronic, and second Foxy Lady got a job in North Carolina which sent the Fox family east. If you look closely you can see the impact of those events on our portfolio pretty clearly.

Because I quit Medtronic all my stock options and company stock developed a “use it or lose it” quality. So I exercised all my options and sold nearly all my company stock. We used that money to help with the downpayment on our North Carolina house (since it took longer than we expected to sell our Los Angeles house). So because of all of that you can see why our Medtronic holdings really fell.

Also, anticipating my leaving Medtronic, I front loaded my 401k to make sure I hit the $18,000 max before I left. Since my 401k was all in US stock index funds (that had the lowest management fee), plus since Foxy Lady’s 401k is similarly all in US stock index funds, that led to the increase in the percentage of our portfolio that is in US stocks. That and the fact that US stocks outperformed international stocks.

Finally, we did add another investment to our portfolio—Lending Club. This definitely deserves its own post, but basically it’s a peer-to-peer lending website (so I grouped it with “Bonds/Cash”). Right now it’s a small amount of money, but Foxy Lady and I have gotten our feet wet and like performance we’re seeing from this investment, so we’ll be increasing it over time.

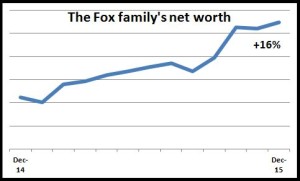

Net worth increase

So all that’s great, but the bottom line is the bottom line. What happened to our net worth in 2015? Fortunately, despite a lower market dragging things down, our net worth was able to grow about 16%.

How is that possible, you ask? Well, it’s just good ole saving money. As I mentioned a couple paragraphs above, Foxy Lady and I both max out our 401k accounts, that being the primary way we save these days. So despite the stock market not being very loving this year, we were able to offset that by putting more money in.

And as two foxes in our late 30s (Foxy Lady just glared and said “37 is clearly still considered mid-30s”), I actually look at this market dip as a bit of a good thing. Using dollar-cost averaging, our 401k accounts were able to buy the same mutual funds we always did, but this time we were able to do so at a bit of a discount from what it would have cost before.

As you all know, I am incredibly optimistic about the future of the US and the world and the stock market. So I know things will go up over the long haul. If in the meantime I can buy some investments on the cheap, all the better.

That’s how we did with our portfolio. The investments weren’t great, but we kept our nose to the grindstone and kept plugging away, which is really the most important thing you can do when saving for retirement. How about you? How did you do in 2015?

Remember that what matters is our long term returns over a lifetime so bear with it! What’s amazing is you were able to increase your beginning-of-year net worth by about 25% this year, and that you did this mostly through savings! With that ability to save you almost don’t need returns on your investment portfolio. Do you have any tips on how you did this, especially in a year when you weren’t working? Does the lower cost of living in the mid-Atlantic deserve much of the credit? Was there a nice upward move in your home value?

Thanks for your question. I was writing a reply and it started to get really long so . . . I figured that could be tomorrow’s post (and the one on 2015’s inflation will just get bumped). So stay tuned tomorrow and I’ll go into more detail.

I’m 37, I’m not old!

So you still don’t think we’re entering into a recession?

I wouldn’t say you’re old as much as . . . there’s really nothing good that can come out of this so I’ll stop there.

As to your question about a recession, if you look at the strict definition which is two consecutive quarters of negative growth, I don’t think there’s much to worry about. The economy is growing, albeit slowly, but it’s still growing.

If you look at a broader definition which takes into account a ton of things like the stock market, employment, capital spending, GDP growth in different sectors, maybe that would say we’re in a recession, but who knows. I’m not too worried.