I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

There was a time when a 7% drop in the stock market in three days would have been a big deal. Now . . . meh.

The stock market peeked last Wednesday and then over the next three trading days promptly fell 7% (and then yesterday recovered about 2%). You’d think that should be notable, but it really doesn’t seem like that.

Why a 7% drop isn’t a big deal

First, this has been a crazy year anyway, so a drop like this just seems like par for the course. In fact, I think that speaks to how crazy things have been that we’re now numb to it.

A 7% drop is actually a pretty big deal. Since 1940 (I didn’t want to include the Great Depression where there were a lot of crazy drops), there have been 28 three-day drops that bad or worse. Is that a lot or not too much?

28 times in 70 years means it averages once every three years or so. That doesn’t seem too crazy. As it happens, we had two such periods in 2020, once in February and again in March. That’s probably not very surprising giving the total stock market meltdown we experienced then. Before that you have to go back to 2015 and before that 2011. That seems to line up with our average; this happens every few years.

But the difference is when this happened before in 2015 and 2011, it seems like we made a big deal of it. Everyone, Stocky included, talked about it a lot, tried to figure out what caused it, and predicted when things would turn around.

This time it just seemed like another couple days. Personally, I think after surviving the Corona stock market, we just expect this now. Down 4% in one day, whatever?!?!? My, oh, my, how far we’ve come (or how far we’ve fallen).

The other thing that made this drop not so bad is it seemed like we were just giving back the gains we made over the previous couple weeks. We lost a lot, but it felt like we just gave back the house money we won a few weeks earlier.

The fall erased the gains we experienced since mid-August. That doesn’t seem like all that big of a deal. Easy come, easy go.

Crazy stock moves is just how 2020 rolls

Nothing about 2020 can really surprise us any more, but how does 2020 stack up to other years. So far, we’ve had major stock market moves (up or down at least 1%) 46% of the time. Nearly half the days have seen the stock market move dramatically—think up or down about 280 points for the Dow Jones.

That happens every once in a while, but what really makes 2020 crazy is that 16% of the days have had CRAZY major stock moves (up or down at least 3%–about 800 points for the Dow Jones). That’s the one that seems remarkable. That means almost once a week, we’re seeing something crazy happen. Wow that’s exhausting.

Historically, 2008 had that many crazy big days (the Great Recession). Before that you have to go all the way back to 1933 and the Great Depression. That puts things in perspective. What we’re going through is crazy, but it definitely feels that we’ve just accepted a heightened level of crazy as our new normal. Sigh.

As always, I remain fully invested and optimistic about the market. I guess I just need to keep some Pepto close at hand.

I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

Probably one of the first things you learned about personal finance when you were a little kid was “Savings Accounts”.

Yet, as an adult, savings accounts are a horrible place to put your money. How can that be? In fact, a savings account could easily be costing you thousands of dollars each year. Yikes!!!

If you don’t have time to read the whole blog, here is your answer: a bond fund gives you 10x more interest with a minimal tradeoff in safety. Okay, there you go. If you interested in understanding my thinking more, here you go.

Crazy low interest rates

Savings accounts today give you an interest rate in the 0.1% range or so. Maybe if you shop around you can get as high as 0.5%, but that’s probably about it.

Obviously, that’s extremely low. We know that stocks historically have an 8-ish% return, but that of course exposes you to the risk that you might lose some of your savings when you need it (more on how big a risk this actually is in a second). Suffice it to say, there are a lot of people who understandably don’t like the idea of having their savings account invested in volatile stocks. Fair enough.

However, you could invest in bonds which are much less volatile than stocks and still get a much higher return that your savings account. Going back to the mid 1980s (which is about as far back as I could easily get reliable data), you can see that bonds have an average return of about 6%. Comparing that to what you could get from a savings account is no comparison.

Just to put some numbers to it, let’s say that you have a nice round number like $10,000 in savings account. You get about 0.3% interest which comes to . . . wait for it . . . $30 per year. Now compare that to a 6% bond; you’d get about $600 per year on average. That’s a huge difference–$50 per month. This decision just paid for your internet bill or your cell phone bill. If you want to get extra nerdy (you never have to ask Stocky that twice), $50 each month for your 40 year investing career would come to about $100,000.

Risk of losing money

Okay. We understand that savings accounts give horrible interest rates. So why do people still use them?

My suspicion is two fold:

They don’t appreciate that there is an alternative to savings accounts called bond funds.

They have an “over-exaggerated” fear of losing some of their savings.

We just took care of #1, so we can’t claim ignorance anymore. Now let’s look at #2. This is a legitimate concern.

We know that stocks move around a bunch (March, anyone?), and historically lose value about one third of the time. Bonds, however, are a much different story. Bonds historically have gone down in value in a given 12-month period about 9% of the time. And just for funsises, if you calculate the average amount bonds go down when they do go down, it’s about 1%.

How does that make you feel? Everyone has different risk tolerances, but to me this is a slam dunk. You can use a savings account and be guaranteed to make a very, very small amount of interest. Or you could take a TINY step up the risk ladder. There you have a 90% chance of doing better, and if you’re unlucky that 10% of the time you’re only losing 1% (about $100 if you have $10,000 in their savings account).

Bond returns (since 1987)

1-year

3-years

5-years

Best

18%

13%

12%

Median

6%

6%

6%

Worst

-4%

1%

1%

% of time losing money

9%

0%

0%

And here’s the kicker. That was just looking at one year. We all know that crazy swings in stocks and bonds become tamer if we allow for more time. At three years, the LOWEST return for bonds was 1% (not negative 1%, mind you, but you’re making 1%). If you push your time horizon out to three years, which doesn’t seem all that unreasonable, at least based on historical performance for the past 35ish years, the worst you could do with bonds is the best you can do with a savings account. The rest is upside.

Irrational fear of losing money

Going back to the questions before, with all this knowledge, why would people still pick a savings account. I think this is a classic example of going with your heart instead of your head. The math is pretty compelling, and making the right decision here becomes a major windfall.

But some people just have a visceral aversion to exposing themselves to the possibility of losing money. I’ve racked my brain and I can’t really come up with serious scenarios where you have a really short time horizon for your savings (less than a year), and you have a really low tolerance for being short as little as 1%.

Maybe if you’re saving for a down-payment on a house you get close, but even then, that tends to be more than a year process and if you are unlucky and come up a bit short, you can just take an extra month or two. Being silly, maybe if kidnappers took your spouse and gave you a year to come up with the ransom, you probably don’t want to risk being short. But then you’re better off getting James Bond or Jason Bourne involved.

Seriously, it’s hard to imagine where the massive trade off in return from a savings account is worth the very small security of being 100% certain you won’t lose money.

Personally, I have not had a savings account since I was in college. We have a checking account for our normal family expenses and then we use a bond fund for shorter-term stuff and then stock funds for long-term stuff.

I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

“Nothing ventured, nothing gained”—Benjamin Franklin

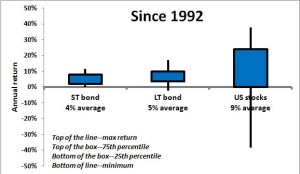

That Benjamin Franklin guy was pretty smart. This is not the first time one of his quotes have landed on this blog. When you enter the world of investing, you need to figure out how you balance the two fundamental, opposing forces of investing: risk and reward. At its simplest, investments compensate investors who take on greater risk with higher returns.

Think of the least risky investment you could make—a savings account. You could invest your money and know that your investment won’t lose money. You could take out the money in a week, a month, or a year; and you would get your original money plus a very small amount of interest. In the US, the risk of you losing money on this investment is 0%. Unfortunately, because there’s no risk, the “reward”, the interest you make, is extremely low: less than 1% currently.

Let’s take a small step up the risk scale—short term government bonds. The chances of you losing money investing in a 1-5 year treasury bond (let’s assume you invest in a short-term bond mutual fund like VSGBX), are extremely low, but it isn’t 0%. There is a chance, albeit small, that changes in the market (interest rates) could decrease the value of your investment. You’re taking on a little bit of risk (since 1988 there has never been a year where VSGBX has lost money), and to compensate for that risk these investments historically tend to return about 1-2%. So you’re being paid a larger return than your savings account because you’re taking on more risk.

Take another step up the risk scale and you get to long-term government bonds and corporate debt (using a mutual fund like VBMFX). These are riskier because there is some chance that you won’t get paid back; this is true for corporate, foreign, or municipal debt. These are also riskier because like their less-risky cousins, the short-term bonds we just mentioned, long-term bonds can change in value due to changes in things like interest rates. The difference with long-term bonds is that the effects are magnified; so if interest rates go up, that would cause the value of your short-term bonds to go down a little, but the prices on your long-term bonds would go down much more. As you would expect, since long-term bonds are a little riskier (since 1988 VBMFX has lost money in 2 years), they tend to return a little more, historically in the 3-5% range.

Now, take a big leap up the risk curve and you get to stocks. Stocks are extremely volatile, especially over the short-term. Since 1930, there have been 24 years (about one-third of the time) where US stocks have decreased in value. It’s definitely a rollercoaster ride. Yet, by bearing the risk that in any given year your investment might go down in value, sometimes down a lot like in 2008 when stocks went down 37%, you get a significantly higher return. Since 1930, stocks have returned on average about 8%.

As you can clearly see in the chart, when you invest in assets with higher average returns (like stocks) you have a lot more volatility in those returns from one year to the next. When you invest in assets with lower average returns (like bonds, especially short terms bonds or even cash), you enjoy much more stability in the value of your investments.

What’s your appetite for risk?

As an investor you need to determine what your appetite for risk is. How will you balance the yin of high returns with the yang of higher risk? At the end of the day, you need to have an investing strategy that allows you to sleep at night. There’s no amount of money that’s worth freaking out every time the market takes a down turn, and it is certain that the market will take down turns. Sometimes it will be a free fall like in 2008 when stocks cratered 37% or it might be a long-term grind like from 1973 to 1978 where stocks fell 23% over the course of 5 years.

That said, a long time horizon is your best friend when dealing with a volatile stock market. While any given year might be crazy, over time there tends to be more good years than bad. Take 2008: in 2008 stocks fell by 37%, and if you needed your money at the end of that year you were hurting. On the other hand, if you had a longer-term investing horizon and were able to stay in the market, all your money would be made back by 2012. In fact, while about 33% of the years have been down years for stocks since 1930, over that same period of there was only one decade, the 1930s, when stocks were down.

So how do you invest? Well, you need to figure out your risk tolerance. Here’s a good way to do that. Imagine yourself as an investor at the end of 2008. You’re in the depths of the financial crisis, stocks are down 37%, and pundits are saying we may be on the brink of financial collapse. What do you do?

Some people like Warren Buffett and Stocky Fox (for important statements I revert to the third person) looked at that as an opportunity to continue to invest in stocks, just now we were buying them at a substantial discount compared to 2007’s prices. In the end our faith was rewarded and we made a killing. However, there were some times when the news just kept getting bad and Pepto-Bismol came in extremely handy.

Others felt burned by the 2008 investing bloodbath and pulled their money out of the stock market to put it in safer investments like bonds or cash. They did so knowing their actions limited their potential for higher returns, but many were willing to accept that if it meant not having to risk their money continuing to disappear into the black hole of the financial crisis.

There’s no right or wrong answer. You just need to figure out where you’re comfortable and invest accordingly. If you’re willing to weather the storms then you should probably invest more in stocks. If you’re more risk averse, then you should probably invest a larger portion of your portfolio in bonds.

Just remember, there’s no such thing as a free lunch. With higher returns come higher risk. If you want safer investments, you have to be willing to give up higher returns.

I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

It certainly looks like the stock market has recovered from the Covid pandemic. Sure, some people may say it will crater again in the fall when flu season hits, but I don’t think it will.

The 2020 stock market seems like a movie. Things started off great and then there was a huge disaster. When things looked their bleakest, we saw things turn around, and in the end we had a happy ending where things were even better than before. Star Wars, Harry Potter, Lord of the Rings, and now the 2020 stock market.

Buried in this roller coaster was a tremendous way to make a lot of money in the stock market. I’m not talking about predicting the future where you had the perfect foresight to sell in February and then buy back on March 23 when things bottomed out. That’s impossible.

However, I am talking about a tried and true method of investing that we talk about all the time-dollar cost averaging.

Dollar cost averaging during Corona

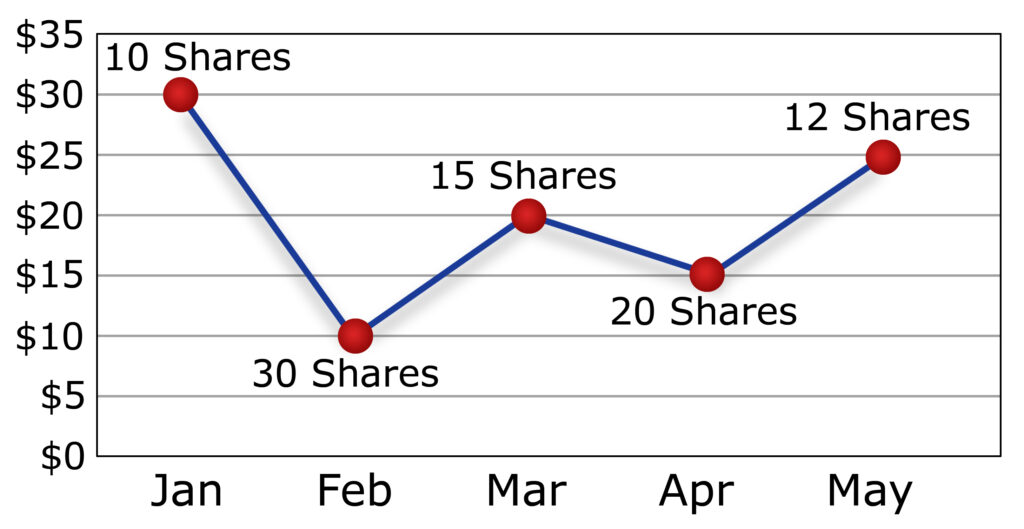

If you need a quick reminder, dollar cost averaging is taking the money you want to put in the market, and investing equal amounts each week or paycheck or whatever.

For example, let’s assume that you invest $1000 per month ($250 per week). If you were able to do that and could keep your discipline, you would have made about $1200. In fact, because of the Corona market crash, you would have made about $900 more than if 2020 had been smooth sailing. Let me explain:

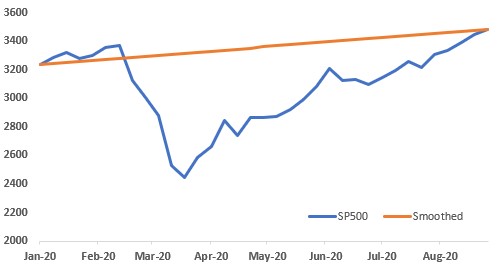

The S&P 500 started the year 2020 at about 3200, and now it’s at about 3500, a bit less than a 10% increase. If we lived in a pretend world where the stock market smoothly and steadily increased from 3200 to 3500 over these past eight months, you would have invested $250 each week and would now have about $9300. That first week you would have gotten so many shares for your $250, and then each subsequent week the stock market would increase, so your overall portfolio would rise in value but the number of additional shares you bought each week would decrease. But hey, you’re up, so that’s good.

However, what really happened, although much crazier and more stressful ended up being better for you at the end of the day. We know that that 2020 stock market wasn’t smooth—it increased early on then had a massive, once in a century crash, after which it had about as steep a V-shaped recovery as we’ve ever seen.

If you were investing that same $250 each week, things would have seemed pretty normal the first two months. However, once March hit the stock market cratered. The value of your investments plummeted which was bad, but the silver lining was that each month you were buying additional stocks at a much lower price. That meant you were getting more shares for each $250 you put into the market.

At the depths of the crisis, if you were able to keep your investing discipline, you were buying stock at about 30% off. Think of it like getting stock from Kolh’s instead of Macy’s; exact same stuff just on sale. Even after the market started its recovery, you were still able to get stocks at cheaper than you would have in that fantasy, smoothed-out scenario.

If you do all the math, it actually adds up to some pretty decent cheddar. Through those eight months, at $250 each week, you would have invested a total of $9,000 (36 weeks). That’s probably not too far off from what you may normally invest in your 401k.

In the smoothed scenario, you would have grown that $9,000 to $9,342, a profit of $342. That seems pretty good given everything we have gone through so far in 2020.

Real life Corona

Pretend smoothed

Amount invested each week

$250

$250

Weeks

36

36

Total amount invested

$9000

$9000

Investment value at end of August

$10,233

$9,342

Investment gains

$1,233

$342

However, in real-life, thanks to dollar cost averaging, you would have grown your $9,000 to $10,233, a profit of $1,233. Obviously, that’s quite a bit more and it speaks to the power of investing discipline.

When things were their worst, in late March, it was hard, really hard, to keep the faith and continue to put money into the market. However, like every other time in the modern history of the stock market, if you were able to follow Rudyard’s advice and keep your head, things came around.

Obviously there’s a moral to this story which is Investing is a long term game. The Corona stock market came and went over the course of a couple months. Things looked terrible but then they improved. If you can stay disciplined, the stock market will give you its riches.

If we as a society truly think Black Lives Matter, then we need to find actionable ways to save the most black lives possible. Deaths of black people by police number about 200-300 annually. Even if you assume all of those deaths were preventable, that is only a minute fraction of the lives that could be saved by black men living with their children and the mothers of those children.

SINGLE-PARENT HOUSEHOLDS (SPH) BY RACE

Nationally, about 35% of US households are headed by a single parent. However, that varies drastically by race. 65% of black households are single-parent, the highest level for any ethnic group. The group with the lowest percentage of single-parent families is Asian and Pacific Islander. Whites are at 24%, American Indians are at 53%, and Hispanics are at 41%.

At a very high level, there is a remarkable correlation between single-parent households and other factors like reflect societal success like income, net worth, crime/incarceration, education.

The data show an obvious trend—Asians are the best ranked along every dimension, followed by whites, then Hispanics, and finally blacks.

Correlation does not equal causation. To reach such conclusions would take enormous, expensive surveys. Even then it might not be possible to tease out all the other important factors and isolate “single parent households”. The rest of the analysis assumes there is a causation. You are free to disagree.

INCREASED DEATHS WITH SINGLE-PARENT HOUSEHOLDS

Intuitively it makes sense that the people associated with single-parent households—both the kids, the parent living with the children, and the parent living without the children—are at increased risk. The biggest culprit is wealth, or lack thereof; single-parent households tend to be poorer and with that comes a myriad of detriments: less healthcare, less nutrition, living in higher crime areas, and many more.

Beyond just the financial component, there are other reasons to think single-parent households increase mortality. For the kids, there’s obvious value in having two parents. Kids are less likely to have accidents if two set of eyes are watching instead of one. Life-skills, especially those taught by a regularly present father may lead to less participation in drugs, crime, and gangs. Depression and suicidal thoughts would seem easier to address with two parental resources rather than just one.

Much of this would apply for the adults as well. The reduced stress of having to be “everything” for the parent with the kids would be reduced. For the parent not with the kids, most often the father, being with his family likely has a positive impact. He has something more to live for and a loving family to come home to—perhaps he takes better care of himself with diet and exercise, engages in less criminal activity, seeks to improve his professional prospects to support the children he sees every day. This is all conjecture and would of course need to be supported by data, but it certainly passes the stink test.

Sadly, the research in this area is sparse and not comprehensive. Also, it is riddled with correlation/causation and other statistical issues. However, the research that has been done statistically significantly concludes that single-parent households lead to premature deaths . . . for all involved. Mortality for children increase by about 40% to 100%, for the parent who lives with the children (typically the mother) by about 50%, and even for the parent not living with the children (typically the father) by about 200%.

Both boys and girls of single-parent families have increased mortality, but this increased mortality is doubled for boys compared to girls. Suicide is about twice as common for single-parent children, with a greater impact on girls than boys. Death due to household accidents is about 40% more common for girls and 270% more common for boys. Death due to addiction is about 400% more common. All really, really sad stuff.

The data also show that the risk among single-parent children, already much higher, is especially deadly for young kids. Infants and toddlers in single-parent households have about a 100% mortality increase while the older kids have a 30% increase.

Reasonable people can debate the precise statistical impact, but the data seems to clearly show these broad trends:

Kids of single-parent households have increased mortality, and it is worse for younger kids and for boys.

Both parents associated with single-parent households have increased mortality, and that worse for the fathers/parents not in the household.

ACTUAL LIVES LOST

We can estimate the annual deaths caused by single parent households. The data is incomplete so we have to make a few assumptions on population size, but those probably don’t have a large impact on the final calculations, and certainly not on the conclusions that single-parent households are leads to thousands of black deaths. The rest is just math that we learned in 4th grade.

Incremental deaths reduced by SPH rate for blacks going to US average

Black kids (4 and younger) in SPH

2.0

0.12%

0.12%

2,400

1,292

Black kids (5 and older) in SPH

6.3

0.10%

0.03%

1,890

1,018

Black mothers (age 19-50) associated with SPH

6.1

0.13%

0.06%

3,660

1,970

Black fathers (age 19-50) associated with SPH

6.1

0.23%

0.46%

28,060

15,109

TOTAL

36,010

19,390

Applying those increased death rates to the populations of kids, mothers, and fathers associated with single-parent households, we get about 36,000 deaths of black people each year due to single-parent households. Assuming that black single-parent household rate fell to the US average, (being reduced from 65% to 35%), that still is over 19,000 incremental black deaths.

Most sobering are the kids. Over 2,300 black kids are dying each year because of greater single-parent households (more than 6 every day). And this is mostly focused on babies and toddlers.

We all want a better world. We all want fewer black people dying. Reforming law enforcement will likely lead to a few reduced black deaths. Increasing two-parent households will save orders of magnitude more black lives, especially the most precious black lives, the black kids.

I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

Sorry for the extended absence from writing the blog. Like many of you foxes and vixens, I have been homeschooling the kits, and that has kept me pretty busy (and on the brink of sanity). The boys started school last week (they go to school two days per week and do remote learning three days per week), so that gives me a little bit of time to get back into the swing of things with my blog.

Picking our way out of the rubble

2020 will obviously be remembered as the year of Covid. They year is not over yet, and we still have a presidential election. But I sure hope that nothing else this year can supplant Covid for the title of “Craziest Crap to Happen in 2020”. I’m a bit nervous.

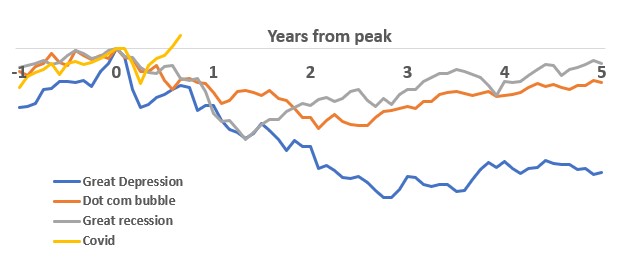

From a personal financial perspective, this was on the Mt Rushmore of stock market calamities, along with the Great Depression, the Internet Bubble, and the Great Recession. At the depth of the freefall in March, the Covid market was actually worse than the Dot-com burst and the Great Recession. And not just by a little bit: Covid was down 20% while Dot-com and the Great Recession where down 13% and 11% respectively at that same point in time.

However, a few months later everything is as good as it was before the nightmare started—actually better. Today, stocks are higher than they were before the Covid hit the fan.

You know how they say “a picture is worth a thousand words”? Here is a picture that shows those four stock markets. Crazy, huh?

We’ll remember this one for a while. In March, the speed and severity of the fall was matched only by the Great Depression. When you have to go all the way back to the Great Depression to find a similarly horrible market, you know you’re dealing with some serious stuff.

Yet, the recovery was arguably more extraordinary. Those other examples had a downward slide measured in years, not months. At it’s worst, the market lost over half it’s value. But what really puts the cherry on top for me is the time it took to recover. Those other markets took years (decades in the case of the Great Depression); Covid just took a couple months.

After 3 months

Nadir

New high

Great Depression

-34%

-83% after 3 years

25 years

Dot-com bubble

-13%

-46% after 2 years

12 years

Great Recession

-11%

-53% after 1 year

5 years

Covid

-20%

-20% at 3 months

7 months

Covid market in perspective

I don’t think in March anyone would have predicted something like this. Personally, I thought we’d be at 3000 on the S&P 500 by July (about 10% down from the market highs). At the time, I thought I was crazy optimistic. As it turned out we were at about 3200, a new high.

That said, this one will leave a scar. No matter how optimistic one is, it will be impossible not to remember that hollow feeling investors had in their stomachs in March. If you were able to keep your head this turned out to be inconsequential. If you sold then you really did yourself a disservice with regard to wealth building.

I imagine that along with the Dot-com and Great Recession, the Covid market will be responsible for thousands of people not participating in the market. They say, “I remember Covid and I just don’t trust the market.” They’ll not invest and really hamper their ability to generate a large nestegg. I suppose we’ll see on all this stuff.

That said, I’m glad we’ve made it out the other end on this okay.

For most investors March could not have ended soon enough. Stocks were down 12.5% (actually I thought it would have been worse, but we’ll talk about that more in a second). Obviously that’s bad, but since 1929 there have been 18 months that were worse.

With emotions running high as the stock market plummets and, more importantly, as the body count from the coronavirus rises, it’s important to use data to put everything in perspective. Let’s dig into what the numbers say.

Ultimately, I am optimistic. Also, as bad as it is right now, it has been worse and we’ve made it through. Hope this post makes you feel better.

Things feel pretty bad right now

As we said above, March was the 18th worst month for the US stock market since 1929. What makes it feel worse is that February was down 8.4%, the 84th worst month. That’s a helluva one-two punch. But even then, this was only the 13th worst two-month period for stocks.

I say all this because what we have gone through has been bad, really bad, historically bad. But it has been worse; many, many times it has been worse. The optimist in me says if we survived all those other times, then we’ll survive this one too.

Light at the end of the tunnel

I have absolute confidence that things will get better, the pandemic will fade, the US and the rest of the world will start making enough tests and masks, and ultimately the stock market will recover. The only question is when.

If you believe, as I do, that the stock market is a good clearinghouse for national/global sentiment on how we’re doing with this pandemic, there is reason to be optimistic. Since April stocks are up 3%, largely driven by yesterday when stocks were up over 7%. Certainly that’s good news, and we all hope that new cases will start to decrease, recoveries will start to increase, and American industry will provide the tools to really finish all this coronavirus business.

Also, as this stretches out, it helps to better and better put what we’re going through into perspective. It has now been almost seven weeks since we were at our stock market high (Feb 19). Since then stocks have fallen 21%. Any guesses how many times this has happened in the past . . . 17. That seems like a lot. In the past 100 years this has happened 17 times. That’s about once every six years. Of course, it’s not nearly that regular. The Great Depression accounted for a lot as did the Great Recession, but still.

Also, as we start to stretch the time horizon out we start to see different periods of history that had similar stretches. We have all the usual suspects: over half of those time periods were in the 1930s, plus one from the dot-com bubble (2002), one from 1987, and one from the Great Recession (2008). But now that we’ve been at this for almost 7 weeks we have a new member to the club: May 1970.

The 1970s were a horrible decade for investing. We had the Vietnam War, oil shocks, the Nixon resignation, sky-high inflation, an ineffectual Jimmy Carter. There wasn’t any one event, but rather that decade was just a long grind of bad.

Let’s wrap this all up. Back a few weeks ago the market was in total freefall and it was scary. But after the initial onslaught things have stabilized. In the past two weeks, the S&P 500 has traded in a fairly tight range (2400 to 2700), so things seem to have stabilized a bit. Now it’s just turning out to be a bad market like the ones we get every generation or so.

Inherent in investing is risk. The psychology of stock markets doesn’t allow the air to seem out of the balloon slowly. Rather, it tends to favor a violent burst. That’s what we’re going through right now. But I do think there is a light at the end of the tunnel.

Making predictions on the stock market it a great way to look stupid. When we first started this, I thought we’d be at 3100 by the end of May. That’s looking less and less likely, but I do think we’ll be at 3000 (down about 10% from our highs) but the time we celebrate the US’s 244rd birthday. We’ll see if I’m right.

Just like you, the Fox family has had to hunker down as we go through this crazy time. I haven’t been able to write a post lately because of a little thing called . . . homeschooling.

Since we’re fully invested, we’ve lost about one third of

our net worth, in line with the overall market decline. In addition to homeschooling we’ve been on

pretty much full lockdown in North Carolina.

A bit more trivially, I am missing out on the NCAA tournament which I

had tickets to and I’m totally bummed that the NBA season is done since I love

watching basketball.

With all that negativity, it’s important that we do try to

stay positive and embrace the upsides that might come from all this craziness. Here are my top 5 investing/financial benefits

that could come from the coronavirus experience.

5. The internet: Everyone knows the internet is bigger than ginormous, but it has really shined. With homeschooling I’ve made a lot of lessons by using the limitless free resources other parents and schools have made available online. The cubs and I do science and geography lessons everyday and youtube is an amazing resource for that.

Foxy Lady and I have been watching shows on Amazon

Prime. Given how much we order off

Amazon, Prime would be a given anyway, but with the shows we’re basically

getting Netflix-lite for free. As it is,

Prime comes out to about $8 a month which seems a screaming bargain.

Pretty much every public library in the country offers access

to download an enormous collection of books for free. I haven’t bought an actual book in probably

10 years, and I haven’t read a physical book in over a year; I just get any

book I want for free on my tablet through my library.

Of course, we knew all this, but I think the pandemic has really highlighted how much is out there and how much is for free. It’s truly astonishing. INFLATION KILLER.

4. Online grocery shopping: When we moved down to Charlotte we were near a Walmart that allowed for online grocery shopping and then you would pick up your order at the store. It’s not home delivery (I think they were just going to start this before the pandemic hit), but it’s still pretty sweet.

I love this way of shopping, and Walmart loves it too. Our grocery bill has actually gone down

because we don’t have impulse buys and we don’t buy things we already have (I

am terrible with that when it comes to cucumbers for some reason). Walmart loves it because it cuts down on

people they need in the store, theft, damage to merchandise, and a lot

more. Everyone wins.

With all the social distancing, I’d like to see this

promoted more. Think of all the infected

people who come shop, touch different stuff, and get others sick. A grocery store is the most necessary of

stores right now so we can’t shut them down, but they are also one that is

infecting people the most. Why can’t

states say if you buy online and pick up without going into the store your

order won’t be charged sales tax? That

would be a helluva bargain compared to shutting down entire swaths of the

economy.

Long-term if more and more people do that, grocery stores

can turn into distribution centers that run much leaner—less space, less people

needed. They save money and pass that on

to us.

3. Euthanizing zombie retail: The pandemic will bankrupt a lot of companies. Broadly, that’s a sad thing, since some of those are going to be good companies that just got swept up in this tsunami.

But there are a lot of companies that will go under that should

go under. They are crappy companies

with crappy business models selling something that customers don’t want. Go to a local mall and you’ll see a ton of

them. Right now they’re dying a slow

death and the chances of them making it are zero.

This business cycle will “put them down” and free up that

space, those workers, that capital to be used on businesses that do make sense

and can work.

2. Changing teaching: Schools closings have forced us to use a completely new paradigm for teaching our students. Actually, the approach to teaching has largely been unchanged for a couple thousand years—students go to a school, listen to a teacher who stands in the front of the room, and there you go.

Sure, in my lifetime, technology has made some inroads, but

compared to other industries the impact has been pretty muted. Look at the role technology plays in your

kid’s classroom (pre-virus) compared to the role it played when we were

kids. Now look at how technology has

totally transformed other industries—purchasing airline tickets, watching

movies at home, consuming breaking news, listening to music, trading stocks,

looking up any possible bit of information you’d ever want to know, and on and

on.

I’m not saying schools in their current form should be

abolished, but there is absolutely a compelling case to make major change. Should there be more home learning? Better distance interaction (see #1)? I don’t know the exact answer, but I do know

that this experience will show that there is a ton of opportunity for

improvement—better educational outcomes costing less money. Like always, those that drive that

improvement will make tons (the US spends about $700 billion on education).

1. Video-conferencing: As I mentioned here, I think there is a ton of potential for video-conferencing to really transform the world in a positive way. Most of corporate America has been told to stay home and telecommute. We still have meetings, still need to interact with people, and still need to get business done. Now we just need to do it remotely instead of face to face.

This is the major opportunity for video conferencing. Right now the technology is kludgy. It’s no where close to what is necessary to

make it a seamless substitute for those in-person meetings. A few of my nerd friends and I got together

for some Dungeons and Dragons action, and it was not ideal (I’d give it a C-).

However, once the technology comes in the demand seems

unlimited. It will create so much value

(think about not having to take a two hour, $500 flight for a 60-minute

meeting). It will also make

collaboration SO MUCH more productive. I

said this could be a trillion dollar opportunity, and now in the teeth of

coronavirus, I think I might have underestimated it by 2-3x.

So there you have it. It sucks what we’re all going through, but we will get through it as a society, no question. More specifically, as investors we’ll come out of this stronger than before; I absolutely believe that.

I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

The insanity of the stock market’s reaction to coronavirus has prompted a few questions in the mailbox. Let’s see what we’ve got.

“Do you think this is a buying opportunity in the market or do you think there is a deeper drop to come?” BB from Greensboro, NC

Actually, the answer is “yes” to both. I do think this is a great buying opportunity,

and I also do think there is probably a deeper drop coming.

Long-term, the market is way overreacting. After yesterday’s bloodbath, stocks are down

about 35% from their highs just a few weeks ago. That seems absurd. All the companies in the world didn’t lose

over a third of their value over this.

Even if you look at the industries that are hardest hit,

like cruise ships and airlines, it shouldn’t be that bad. Maybe they’ll be out of commission for a

couple months, and that’s bad, but not 35% bad.

Other industries shouldn’t be nearly that bad. Grocery stores should be doing just fine

(better than fine given the rush to buy toilet paper and hand sanitizer). They’ll have a little bit of disruption while

we work our way through this, but it should be fairly minimal. That’s all to say, I think things are way

oversold and in a year or two we’ll look at this as an amazing buying

opportunity.

However, in the here and now I don’t think we’re out of the

woods. There’s so much still unknown, most

importantly “when we’ll reach peak infection in the US”. That’s really the key to it all. South Korea reached peak infection after

about two weeks while Italy still hasn’t reached peak infection after three

weeks. Either way, the stock market will

recover. If we look more like South

Korea then we will recover nearly as quickly as it’s fallen. If we look more like Italy then we will fall

considerably more before things turn around.

To directly answer the question, I would buy into stocks but not right now. I think things are going to get worse before they get better. There’s a famous saying in investing: “don’t try to catch a falling knife”. Basically, it means when a stock is falling, don’t try to time it perfectly. Rather wait until the stock “hits the floor” and things settle. Even if you miss the absolute bottom by a bit, you’ll still be able to get in when stocks are well off their highs.

That’s the approach I would take now. I would keep any cash handy and wait until we

confirm we’ve hit peak infections. Once

that happens, the stock market will probably rally 10% or so in a single day. You’ll miss out on that but you’ll still be

able to get in at 20-30% less than what you would have gladly paid a month ago.

“Why is gold going down? With trillions of dollars reduction in equity, where is all the money going? Is it liquid, and will it come roaring back when the virus caused business slowdowns stop?” Uncle Bobcat from Ft Wayne, IN

Gold has been pretty interesting through this. It was steady to rising for most of the

crisis and it was only in the past few days that it started a freefall similar

to stocks.

The light blue line is gold and the dark blue line is the US stock market

The short answer is that gold has been falling because interest rates have been cut. Look at gold’s major falls on March 2 and again yesterday, and those coincide with when the Federal Reserve cut interest rates.

The longer and more interesting answer is that I don’t think

it’s clear what role gold plays in this crisis.

In 2009 everyone thought the world economies were going to collapse and

fiat currency would become worthless paper.

Hence, people were fleeing to gold as a store of value.

That doesn’t seem to apply here. I don’t think anyone feels the economy is

going to collapse in some cataclysm.

Rather, the economy is just taking a massive body blow. Things that were worth X before are now worth

X less 20-30%. That goes for stocks for

sure but then for a bit of everything else like shiny yellow metal.

With regard to your last question, I do think things are

oversold and things will be better. As I

said in the other question, everything revolves around when we hit peak

infection. Once we hit peak infection, I

think we’ll have a huge recovery.

That said, I don’t think we’ll get back to where we were

before this all started, and that should make sense. A huge amount of value has been lost that we’ll

never get back. Those idle cruise ships

can never make up that time. Same

applies to restaurants, conferences, sporting events (I know a part of Uncle

Bobcat died when they cancelled the NCAA tournament). That value’s gone and can’t be recovered.

On the other hand, a lot of stuff can be made up. A lot of the supply chain problems caused by

China not shipping stuff will be made up once the factories start humming

again. Same thing with dentist visits, plumbing

work, and other stuff like that.

Take all that into account and my sense is that within a year

we’ll be at about 3-5% below where we were when all this stuff started.

I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

Holy Crap!!! That’s

really the only appropriate response to the craziness of the stock market over

the past few weeks. So over-the-top has

been said craziness that I just couldn’t sit on the sidelines any more. I had to get my stocky back on.

Let’s dive in with what’s really going on, how crazy is all this really, and if you should be freaking out?

The numbers

Let’s try to remove emotion from the craziness of the stock

market for the past few weeks and just look at the facts, the numbers.

On February 19, the stock market* peaked at 3386. The next two days it fell a bit, but then on

Monday, February 24, it slipped over 3% and the freefall began. Since then it has plummeted to 2711, a 20% decrease. That’s a crazy fall but let’s put that in

perspective.

First, before all this began, the stock market was up a bit

less than 5% for the year (not bad for two months). So really we’re just down about 16% year-to-date. That’s certainly not good, but being down 16%

feels better than being down 20%.

Second, despite all of this, we are up about 9% from where

we were at the beginning of 2019. Going

back five years, and the market is up about 32%.

You get my point. This is definitely bad, but I think one of the things that makes it so bad is that the pain has been so focused. Who knows what next week will bring (I am writing this Sunday night after the cubs finally went to sleep). Maybe the market is taking another dump on Monday morning as you read this. But those historical numbers seem decent. If someone told you at the beginning of 2019 that stocks would be up almost 10% over the next 15 months, I think you’d probably take it.

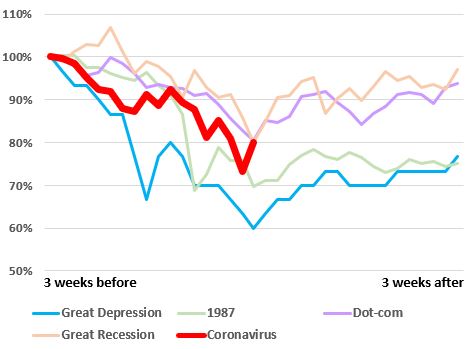

Historic context

The past three weeks (17 trading days) have been bad, even

by historical standards. But how bad

really?

In the past 17 days we are down 20%. Since 1928, there have been 15 other periods

that bad or worse. Over 90 years, this

has been worse 15 times. That doesn’t

seem all that bad, actually.

Of course, that doesn’t mean this happens every six years or

so. It’s much more lumpy. As you would probably guess, most of those 15

periods come from the Great Depression, eight of them in fact. That accounts for half of those

instances. Needless to say, the Great

Depression was a colossal

economic calamity the likes of which we’ve never seen since. This is not going to be another Great

Depression. Not anything remotely close

to that.

The others are a smattering of instances around World War II

(1937, 1938, 1940, 1946), the biggest single day fall in the stock market’s

history (1987), the dot-com bubble (2002), and the Great Recession (2008,

2009).

This time seems a bit middle of the road compared to those mega-examples. The graph shows the stock market in the three weeks before the you-know-what hit the fan and the three weeks after. What we are going through today is in the bright red line.

This gives me a bit of comfort. Coronavirus had a steeper fall than most, after

three weeks (where we are today), it was as good or better than any of those

examples. In the following three weeks

thing improved in every case (for the Great Depression it got a bit better as

you can see, but then the bottom really fell out).

Of course, it’s impossible to predict the stock market, but I tend to think things aren’t nearly as bad as the stock market’s performance would lead you to believe. Let’s say I’m 70% optimistic and 30% pessimistic.

The argument for stocks recovering quickly

If you compare what we’re going through to the dot-com

bubble and the Great Recession, I think we’re in a lot better shape.

In each of those examples, there were fundamental and

systematic problems with the stock market and the economy. In 2002 there was rampant accounting fraud (Enron,

Worldcom, Qwest, etc.) that made it impossible to invest based on trustworthy

information, the lifeblood of the stock market.

In 2009 the banking system was collapsing, threating to grind the wheels

of commerce in the US to a halt.

Coronavirus just doesn’t seem all that bad in

comparison. Those were deep, dark issues

that took a long time to unwind and correct.

That doesn’t seem to be the case here.

In the next few weeks the number of new cases will peak. Social distancing, warmer summer weather, and

the miracles cooked up by the pharmaceutical industry are going to fix this.

If you look at data from China (not a good idea since I don’t

trust their data) and South

Korea (I trust their data more), this doesn’t last very long. South Korea started getting cases on February

19, and the US started getting cases on March 2; so we’re about two weeks

behind them. Their new infections peaked

on March 3; if ours follow suit we should be peaking this week. Even if it takes us twice as long to peak,

that’s only another few weeks. That

doesn’t seem all that bad.

Things are starting to turn for Koreans positively in other

ways too. People are starting to recover

to the point where the total number of people infected is flat—every day just

as many people are considered fully recovered as there are new cases. Also, their death rate is falling precipitously.

Even if it takes us twice as long to peak and then flatten

as it did in South Korea, that’s only another few weeks. That doesn’t seem all that bad. It’s definitely better than the Armageddon scenario

that seemed to be priced into the market right now.

Going into this, the economy, especially the US economy, was

quite strong and there’s no real reason to think that will change. Banks aren’t going to start much stricter

lending regulations as was the case in 2009.

You don’t have entire industries that we thought were very profitable

and now we know are unprofitable as was the case in 2002.

Once we get the all-clear, there’s no real reason to think things won’t go back to normal, or maybe even better than normal as we work off some of that pent-up demand.

The argument for stocks still facing trouble

As optimistic as things look for South Korea, they look that

bleak for Italy. Italy got their first

cases a few days after South Korea, but they have yet to peak. Everything is on total lockdown and there isn’t

an end in sight.

If we end up looking more like Italy than South Korea, that’s

bad, obviously. Reasonable people can

debate which is the better analog.

As it stands, in the US, the hits keep coming. Major components of industry are shutting

down (mostly sports, travel, tourism, and conventions). Very honestly, this became real for me last Wednesday. That’s when the NCAA announced fans wouldn’t

attend the basketball tournament (I had tickets) and the NBA cancelled the

season (the NBA playoffs are my Christmas).

On Friday we started an international travel ban. Yesterday our state joined many others in

cancelling schools for kids.

There’s an obvious human cost to all that, but there’s also

an economic cost, one that will never be recovered. You can’t get the revenue for those tickets

back, enjoy those cancelled cruises, fly on those cancelled flights. That’s all gone. At a minimum that’s probably 3-5% of the

value of the stock market.

And that’s if things go right. There’s a lot of reason to believe that other

industries might need to shut down. There’s

also a lot of reason to believe that this might take months rather than

weeks. As those things happen, it will

get worse for stocks.

So there you go. That’s my take on all this crazy coronavirus mayhem. Sadly, this has given a lot of material for future posts, so you should expect another post from me on Wednesday. Ha, ha!!! That’s not sad, that’s great news.

*Unless otherwise stated, I’ll be using the S&P 500 when

I refer to “the market”. For stock data

before 1950, when the S&P 500 began, I am using a “proxy” of the S&P

500 that Yahoo!Finance has created going back to 1928.