I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

SPOILERS WARNING

Between the gore and the incest, there are some valuable personal finances lessons from A Game of Thrones. This Top 5 list is dedicated to all those who fell fighting for the living against the Night King.

5. Debt creeps up on

you: King Robert’s reign was a

largely peaceful and prosperous one. Yet

like so many people, Robert overspent and went into debt. It wasn’t any one thing and at first he

really didn’t seem to notice. However,

before too long Robert was hamstrung by his debt, and it force him to make bad

choices—the terrible marriage to Cersei being forced upon him since the

Lannisters held most of his debt.

That marriage to Cersei: we all know how that turned out for

Robert. Oops.

4. Everyone likes to

look richer than they are: Rather

ironic based on #5, but by season 4 the Lannisters are broke. Their gold mines stopped producing and they

are deeply indebted to the Iron Bank.

Sounds pretty dire, but you wouldn’t know it by looking at

them. They are still “rich as a

Lannister” and give the outward appearance that they are rolling in the gold

dragons. In no way do they let that they

aren’t rich as ever, and why would they?

Who would want to show their rear end to others?

3. “How would we know

we can’t fly unless we leap from some tall tower”: Euron Greyjoy is one of the creepiest dudes

in the series, but I love this line.

Life is about taking on risk, understanding it, and making

decisions that give you the most upside for the risk you take. This is especially true with investing.

The key is taking smart “leaps,” those where the rewards

more than offset the risks. Stocks

definitely fall into that category.

2. “Power resides

where people think it resides”: Here

Varys speaks one of the most important lines in the entire series.

There’s probably no statement that describes our financial

system better. Banks work because people

have think they work—you put your money in and you get it out. Fiat currency is really just paper with

colored ink, but they work because people think they can reliably use those

pieces of paper to get other stuff.

The best, most recent example has been Bitcoin. For a while people thought Bitcoin was really

valuable so it went up to $19,000 (Dec 2017).

Then all the sudden people didn’t think it was valuable so it plunged

down to $3200 (Dec 2018), and now it’s back up to $5300. Nothing has really changed about its value or

intrinsic net worth except what people think

about its value.

1. Being good at personal finance opens up A

LOT of opportunities: Littlefinger

was my absolute favorite character, and he’s a great example of the power that

comes with being really good with personal finances.

He started out as a nobody and rose to arguably the most

important and richest person in the seven kingdoms. How did he do it? Investing well and being good with

money. He “had a gift for rubbing two

golden dragons together and breeding a third.”

In our world financial literacy is abysmal. Those who can master those skills can do

quite well; the average salary for a financial planner is over

$100,000. Smart financial decisions

can make a millionaire out of nearly anyone.

As Littlefinger shows, the sky’s the limit with this skillset.

A few years back, I wrote a blog comparing the financials of renting versus buying your house. Back then renting came out ahead when you just looked at the dollars, which was a bit surprising. It seemed to buck conventional wisdom that buying is also the best option.

This seems especially important in light of some of the tax changes that impact your mortgage and property tax deductibility.

For this post, I want to look at the choice from a purely financial perspective. And what better way to do that than break it down Dr Jack style? Just to put a little meat on the analytical bone, let’s assume we have a home that we could buy for $400,000 or we could rent for $2000 (I did a quick search on Zillow in a few different markets and this seemed reasonable).

UP-FRONT COSTS: When you rent, you have to give a deposit which is typically something like one month of rent, so that’s $2000. Not a big deal in the grand scheme of things. When you buy, your down payment is in the range of 20% (or maybe even higher since the 2008 financial crisis—the Fox family had to put 25% down on our house). That would mean $80,000 if you’re buying.

At first glance that may not seem like a big deal because it’s still your money, it just happens to be “invested” (did you notice how I used quotes there?) in your home. However, when your $80,000 is tied up in your house you can’t invest it (no quotes there) in the stock market. Since the stock market historically returns about 6% that means you’re passing up $4800 per year on average. Over an investing career that ends up being a TON of money.

Advantage: Bid advantage to RENTING

RISING INTEREST RATES: We’ve been living the last decade with historically low interest rates. A 30-year fixed loan was in the 3.5% range, and all was well. Since then interest rates have steadily crept up.

The math on interest rate increases is pretty powerful. A 1% increase would increase your monthly mortgage payment about $3200 per year or about $280 per month.

A couple months ago, interest rates rose to about 5%, but since then it has settled down to about 4%. Either way, interest rates are going up, and it seems that will probably be the long-term trend.

Advantage: RENTING

MONTHLY PAYMENT: The most common knock I hear on renting is “every month you pay rent, you’re throwing that money away.” I hate that comment, and part of this post is to show how little sense that makes. Obviously when you are renting, your monthly payment is your rent, $2000 in this example.

When you buy, your monthly payment is your mortgage (here we aren’t going to include insurance and taxes, that will come later). If you have a typical 30-year mortgage, let’s say at 4.5% interest, your payment is going to be about $1620 per month. That’s quite a bit less than you’re paying in rent, so obviously that’s an advantage for buying, but then there’s another little bit of good news. That $1620 you’re paying is mostly interest, but a small amount is going towards paying down your loan. In a way that can be seen as you “saving” money. In this example the amount going towards you’re loan would be about $200 per month. So that’s pretty nice. Of course that “forced savings” has a low return compared to the stock market, so it’s not as good as it could be.

Of course, that means that about $1400 per month is going to interest. So when people say that you’re throwing away your rent, can’t you say the same thing for the interest on your mortgage? Either way, this is definitely an advantage to buying.

Advantage: BUYING

OTHER COSTS: With renting, once you pay that rent check, you’re pretty much done. With buying you have a lot of other expenses that nickel-and-dime you to death. Property taxes have to be paid (let’s say 1% of the property value so that’s $333 per month). If you live in a condo complex or an association you might have monthly dues that could range from pretty minor to a significant chunk of money (when the Foxes lived in a condo in downtown Chicago, our monthly association fees were $900 per month—ouch!!!). Those can definitely add up, so that’s a nice advantage to renting.

Advantage: RENTING

TAX ADVANTAGES: This is where a huge change has happened recently. Before, all your mortgage interest and property taxes were tax deductible. Now there is a $10,000 limit on those deductions. In a lot of scenarios, your property taxes won’t be tax deductible. Because of the higher standard deduction, a lot of times it won’t make sense to deduct your mortgage interest either.

Before, the deduction for your mortgage interest and property taxes might be worth about $600 per month. Now that is certainly less, maybe all the way down to nothing.

Advantage: WASH

INFLATION: Once you buy your house your biggest cost, your mortgage, is going to stay put. We’ve talked about inflation before, and the enormous impact that even a little inflation can have on expenses after many years, so this seems pretty awesome that you don’t need to worry about it for your biggest expense.

With rent “that’s where they get you”. Rents almost always go up. Often there are laws that put a cap on how much they can go up, 2% seems a number I’ve heard before, so that provides some relief, but even that 2% can be a big deal. If today your rent is $2000, in 10 years it would be $2440, in 20 years it would be $2970, and in 50 years it would be $5390. That sucks, especially when compared to buying where your mortgage payment will always stay the same.

Advantage: Big advantage to BUYING

SELF-DETERMINATION: A neighbor was renting a few houses down from us. The family loved the house, loved the neighborhood, loved the neighbors (of course they did). But one day the landlord called her and said she wasn’t renewing the lease because she (the landlord) was moving into the house. That family that was renting was FORCED to move even though they didn’t want to. That sucks.

When you rent, you’re definitely at the whim of your landlord. If you buy, you are in control of your own destiny, baby. Get drunk off that power.

Advantage: BUYING

UPKEEP: One of the super-nice things about renting is that you don’t need to worry about when things break down. If there is a problem with the toilet, call the landlord. Water damage from the really bad storm, call the landlord. Fridge on the fritz, whatever—call the landlord. In general this is an awesome advantage. This is even better if you’re not a very handy person.

If you own a home, whenever anything goes wrong you need to fix it yourself (hence my “handy” comment) or worse you have to pay someone to fix it for you. There’s no perfect estimate, but a generally accepted rule is you should plan on spending 1% of the home’s value on maintenance. In our example that would be about $4000 per year.

Advantage: RENTING

NICENESS: As an owner, if you want to make your place nicer you absolutely can. If you want a pool, build it; hardwood floors, install them; custom closets, wallpaper, nice landscaping, and on and on. As a renter there’s a reluctance to do it because in some sense you’re paying to make someone else’s property nicer. If you rent there for years and years, maybe that’s not a huge deal, but that “self-determination” issue rears its ugly head.

I don’t have statistics on this, but I bet that most renters would love to make their place nicer, but just don’t because there is some deep attitude that you don’t do that when you rent. I totally get it and understand it, but it sucks that this keeps you from making your place as nice as it would otherwise be.

Advantage: BUYING

WORST-CASE SCENARIO: I’m not talking about your hot-water heater going bad or having to replace the roof (those we captured in “Upkeep”). Here I’m talking about real worst case scenarios like a natural disaster (in California earthquakes aren’t covered by most homeowners insurance policies; you can get earthquake insurance which is really expensive, so most don’t get it), or the neighborhood really turns bad, or termites or black mold infestations happen inside the walls. Let your imagination run with this for a second and you can really think of some nasty stuff.

As a renter, you can pick up and leave the nightmare behind. Just go somewhere else and start paying someone else rent, and problem solved. Not so if you own the home. Your single largest investment is at risk. Sucks to be you.

By its nature, the worst-case scenario isn’t very likely, but still it could happen. This is one of the things that keeps me up at night as a homeowner.

Advantage: RENTING

ASSET ALLOCATION: A mortgage is a “forced savings” program in a way. Every month you’re making a mortgage payment and part of that goes towards your equity that you can use as you get older (reverse mortgages, cash-out refinances) or pass on to your heirs. After 30 years your house will probably be paid off and you’ll have a tidy little sum of cash to supplement your portfolio. Also, because home values tend to be much steadier than stocks, in a way this investment might seem like a bond.

We saw how crazy important asset allocation is, so if you have a lot of home equity, that might make you feel more comfortable to put a bigger portion of your portfolio into stocks which historically have a higher return. This is a bit of a tricky one, but there’s definitely some level of advantage there.

Advantage: WASH

REALTOR COSTS: There will come a time when you are ready to leave your current home and move somewhere else. If you’re renting this is easy (but not super-easy). Usually, you’ll wait for your lease to expire and then head on down the road. If you need to move right away and your lease isn’t up for a while, that can create a bit of a challenge of breaking you’re lease. That could be as easy as paying a penalty of a month’s rent, or your landlord could play hardball and hold you to your lease until the end. So this can be a pain, but more in the “moderate” zone.

When you own a home and have to sell it, that is a monumental undertaking. Getting a home ready for sale, listing it, showing it, and ultimately closing the sale can take months from beginning to end. Also, it’s not cheap. While realtor fees vary, they average about 6% of the home’s value. In our little example that would be $24,000. That is a lot of money. If you’ve been in the house for 30 years, that will amortize to less than $1000 per year, but if you’ve only been living there a few years that could be thousands of dollars per year that you need to tack on the to “Buy” expense column.

Advantage: Big advantage to RENTING

PRICE APPRECIATION: We saved the best for last, kind of. When you own your home, you get to take advantage of any price increases that your home experiences. Of course, if your home goes down in value, you suffer those loses too. However, like stocks, homes have historically increased in value over time, with notable exceptions like when home values crashed in 2008.

That’s great news, right? No question. However, it’s not as good as most people think. You hear all sorts of crazy stories about people making a killing off their house, but those tend to be anecdotes rather than the rule. The numbers are hard to come by but I think the most definitive and well-respected data, the Case-Shiller index (developed by my BFF Robert Schiller) shows that prices for existing homes have only increased 0.5% over the past 40 years after you account for inflation.

THAT’S CRAZY. That goes against everything we hear. How can that be? Well his index controls for things like home sizes getting bigger, houses getting nicer features, etc. So it really tries to do an apple-to-apples comparison of what you can expect will happen to your home. So home prices do tend upward, but just not at anywhere near the pace that we’ve come to believe.

Advantage: BUYING

Buy

Rent

Investment return on down payment

$400

Interest/rent

$1,333

$2,000

Property taxes

$333

Tax advantage

$0

Maintenance

$333

Realtor fees (5 years)

$400

TOTAL

$2,800

$2,000

If you put it all together Buying “loses” with a score of 5-6-2. Furthermore the math shows that Renting comes out ahead on a monthly expense basis, and it has become an even bigger advantage with the new tax laws. Yet, Buying wins on a lot of those intangibles. Ahhhh, this is why the decision is so complex. Hopefully you saw my point that buying isn’t the unambiguously better option.

If you look at the numbers, it really breaks down to two major factors—realtor costs and price appreciation. The longer you’re in your home, the more years you can spread that 6% realty fee over. So if you’re planning on moving after a few years, that becomes a major disadvantage to buying. Your home appreciating in the icing on the cake that can really make the whole difference. However, the Case-Schiller index showed that prices don’t rise nearly as fast as everyone seems to think (hence, I didn’t even include it in the expense comparison).

It’s a tough call, but the dollars are real. Renting costs about $800 less than Buying in our example; that 40%!!!

The Fox family owns our home, and it has turned out to be the best investment we’ve ever made. We bought in 2010 when the housing market in Southern California had been thoroughly thrashed by the 2008 crisis. In the past 5 years our home has rebounded, more than doubling in value. We would have missed all that had we rented, but if I’m honest with myself, it was just really lucky timing. Sometimes it’s better to be lucky that good.

Long before there were ever stocks or bonds, the original investment was gold. Heck, even before there was paper currency or even coins, gold was the original “money”.

That begs the question, What

role should gold have in your portfolio?

If you don’t want to read to the end, my quick answer is “None”. However, if you want to have a bit of a

better answer, let’s dig in.

Gold as an investment

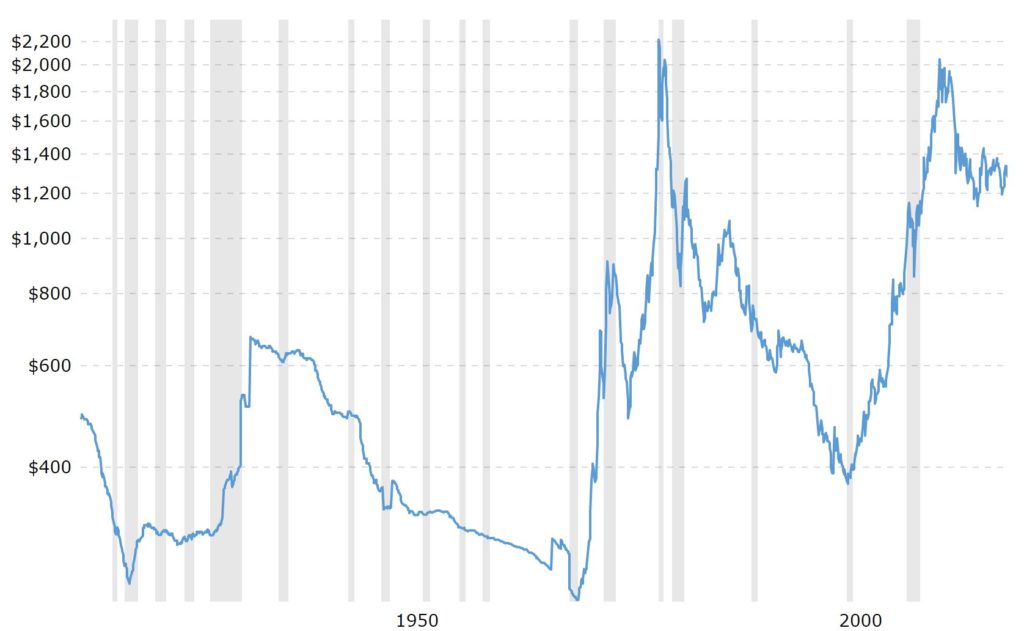

Just like stocks and bonds, gold is an investment. The idea is to buy it and have it increase in value. Makes sense. And historically, it seems to have been a good one—back in 1950 an ounce of gold was worth about $375 and today it’s worth about $1300. Not bad (or is it???).

However, there is a major difference between gold (and broadly commodities) as an investment compared to stocks and bonds. Gold is a store of value. If you buy gold it doesn’t “do” anything. It just sits in a vault collecting dust until you sell it to someone else.

That’s very different from stocks and bonds. When you buy a stock that money “does” something. It builds a factory that produces stuff or it buys a car that delivers goods or on and on. What ever it is, it’s creating something of value, making the pie bigger. That is a huge difference compared to gold, and it’s a huge advantage that stocks and bonds have over gold. You actually see that play out by looking at the long-term investment performance of gold versus stocks.

Golden diversification

Statistically speaking, gold gives an investor more diversification than probably any other asset. We all know that diversification is a good thing, so this means that gold is a great investment, right?

Well, not really.

Stick with me on this one. Gold

is negatively correlated with

stocks (for you fellow statistics nerds, the correlation is about -0.12). Basically, that means when stocks go up gold

tends to go down, and when stocks go down gold tends to go up.

Over the short term, that’s probably a pretty good thing, especially if you want to make sure that your investments don’t tank. In fact, that’s one of the reasons gold is sometimes called “portfolio insurance”. It helps protect the value of your portfolio if stocks start falling, since gold tends to go up when stocks go down.

However, over the long-term, that’s super

counter-productive. We all know that

over longer periods of time, stocks have a

very strong upward trend. If gold is

negatively correlated with stocks, and if over the long-term stocks nearly

always go up, then that means that over the long-term gold nearly always goes

(wait for it) . . . down.

That doesn’t seem right, but the data is solid. Look back to 1950: an ounce of gold cost

$375. About 70 years later, in 2019,

it’s about $1300. That’s an increase of

about 250% which might seem pretty good, but over 70 years that’s actually

pretty bad, about 1.8% per year.

Contrast that with stocks.

Back in 1950 the S&P 500 started at 17, and today it’s at about

2900. That’s an increase of about

17,000%, or about 7.7% per year. WOW!!!

Just to add salt in the wound, inflation (it pains me to say

since I think the data

is suspect) was about 3.5% since 1950.

Put all that together, and gold has actually lost purchasing power since

1950. Yikes!!!

A matter of faith

Fundamentally, if you have faith that the world will continue to operate with some sense of order, then gold isn’t a very good investment. So long as people accept those green pieces of paper you call dollars in exchange for goods and services and our laws continue to work, gold is just a shiny yellow metal.

However, if society unravels, then gold becomes the universal currency. The 1930s (Great Depression), the 1970s (OPEC shock), and 2008 (Great Recession) were all periods where gold experienced huge price increases. Those are also when the viability of the financial world order were in question. Each time, people were actively questioning if capitalism and banks and the general financial ecosystem worked.

People got all worked up and thought we were on the brink of oblivion. Gold became a “safe haven”. People knew no matter what happened, that shiny yellow metal would be worth something. They didn’t necessarily believe that about pieces of paper called dollars, euros, and yuans.

Yet, the world order hasn’t crumbled. Fiat currencies are still worth

something. Laws still work, so that

stock you own means that 1/1,000,000 of that factory and all it’s input belongs

to you. Hence, gold remains just a shiny,

yellow metal.

The bottom line is that stocks have been a great long-term

investment, and gold hasn’t. And that’s

directly tied to the world maintaining a sense of order. So long as you think that world order is

durable and we’re not going to descend into anarchy Walking-Dead style, then gold isn’t going to be a good investment.

So the survey says: “Stay away from gold as an investment in

your portfolio.”

In the United States, Social Security is an important part of most peoples’ retirements, actually probably too important in many instances. Social Security is a fairly simple program that was designed to be pretty idiot-proof. You don’t really need to make many decisions for it, which contrasts sharply with all the decisions you need to make on your other investments (like tax strategies, asset allocation, picking investments, etc.).

With Social Security, you just work and the government takes its 12.4% (6.2% from you and 6.2% from your employer) of your compensation. In fact, you don’t really have a choice in the matter and the government does it automatically. Then when you get old, the government gives you a monthly pension. Not real complicated on your end.

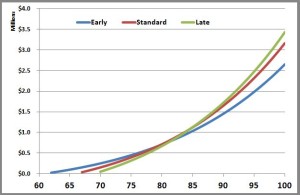

However, there is one really important decision you need to make regarding Social Security: when you start taking it. Basically, you have three options: 1) Early retirement-when you turn 62; 2) Regular retirement-when you turn 67 for most of us; 3) Late retirement-when you turn 70. And as you would expect, if you start taking Social Security later, you get a larger monthly check from the government.

This is obviously an important choice to make, and it’s one that gets a lot of press coverage with all sorts of people opining on what to do (I guess with this post, I am adding my opines to those ranks). Generally speaking, the advice slants towards taking it later. Yet, I wonder if that’s really good advice. Using my handy-dandy computer, let’s go to the numbers to see what they tell us.

I checked my Social Security statement and I’ll be able to pick from one of the three choices:

Age to start taking Social Security

Monthly check

Early retirement—age 62

$1800

Full retirement—age 67

$2600

Delayed retirement—age 70

$3200

As you would expect, the answer to this riddle is a morbid one. When do you expect to die? The longer you live, the more it makes sense to delay taking Social Security so you can get the bigger check. That’s not a tremendous insight, but when you do the math, you start to see some interesting things going on. I fully appreciate that Social Security is very nuanced and complex, so I am just covering the simple basics here.

In my analysis to be able to compare the different scenarios, I assumed that I saved all the Social Security checks and was able to invest them at 4%, about the historic rate for a bond. If you do that the table above expands to this:

Age to start taking Social Security

Monthly check

Highest value

Early retirement—age 62

$1800

Die before age 79

Full retirement—age 67

$2600

Die between age 80 and 84

Delayed retirement—age 70

$3200

Die after age 85

That’s pretty profound actually. The average life expectancy in the United States is 76 for men and 81 for women. Doesn’t that mean that most of us should be taking Social Security with the early option? That contradicts most of the advice out there on this topic. That, ladies and gentlemen, is why Stocky is here for you. This is where it starts to get fun, and we can apply a little game theory (awesome!!!).

When to start Social Security?

Actually, once you reach age 62, the life expectancy of those still alive (and able to make the decision on Social Security) is 82 for men and 85 for women. This makes sense because you’ve survived to 62 so by definition you didn’t die before then (awesome insight, Stocky), and those early deaths pull down that initial life expectancy model.

Since women are better than men as a general rule (Foxy Lady took over typing for just a second there), let’s look at this decision as a 62 year-old-woman. She needs to make a decision on when to take Social Security. She knows her life expectancy at this point is 85, which means there’s about a 50% chance she makes it to 85. So the worst choice for a 62 year-old is to take the early retirement option. She’s probably going to live long enough that either full retirement or delayed retirement is the better option.

At 62 she does the smart thing, and decides to wait. Her next decision comes at age 67, assuming she lives that long (there’s about a 5% chance she’ll die during those five years). But a similar thing happens—when she was 62 her life expectancy was 85 (right on the border of picking between full retirement and delayed retirement), but now that she’s 67 her life expectancy jumps up a year to 86. So if she makes it to 67 then she’s better off taking the delayed retirement (of course, there’s about a 4% chance she’ll die before she makes it to 70).

That’s a little bit weird though, isn’t it? It kind of feels like you’re that horse with a carrot dangling over his head, keeping him walking forward. It’s a bit of a conundrum. At any given time, you’re better off delaying starting your Social Security, so the math tells you to keep waiting and waiting. But if the dice come up snake eyes and you die, then you miss out on everything (not strictly true, but true enough for our analysis).

And keep in mind that since Foxy Lady hijacked Stocky’s computer, we’ve done this analysis for women. The math tells you that it’s just about a wash between taking Social Security at 67 or 70. Since women live on average 3 years longer, for men you would think it means that the advantage leans towards taking it early.

What does it really matter?

So the analysis tells us that we’re better off waiting if you’re a woman and it’s really close if you’re a man. And of course the longer we wait, the further we come out ahead by taking delayed retirement instead of early or full retirement. But how big of numbers are we talking?

Remember, the cut off for when full retirement becomes better is at about 80 years old. The cut off for when delayed retirement becomes better is about 85 years old.

Future value of Social Security payments

Age

Early retirement (62)

Full retirement (67)

Delayed retirement (70)

85

$1,031,256

$1,119,603

$1,125,233

90

$1,450,231

$1,644,630

$1,716,663

100

$2,647,751

$3,158,200

$3,431,844

Those are meaningful differences. If you make it to 100 years old, delayed retirement comes out about $800,000 higher than early retirement. However, those are in future dollars, 38 years into the future if you’re 62 today and faced with this decision. That $800,000 when you’re 100 would be worth about $370,000 today. Of course that’s if you make it to 100, which isn’t really likely (about a 3% chance).

If you make it to 90 years old (you have less than a 30% chance) then the difference is about $260,000 in future dollars which is about $150,000 today.

Wrapping up, I’m really torn on this. There’s a little bit of a prisoner’s dilemma type thing working that keeps making you want to push back when you start collecting. And then when you look at the upside of delaying retirement, the numbers are pretty big (whenever you’re talking about hundreds of thousands of dollars, that’s real money), but the chances of us making it to that super-golden age are pretty small.

I suppose it’s best to wait, but I’m giving that a pretty “luke-warm” endorsement. It certainly isn’t the “slam dunk” that so many pundits make it out to be.

Actually, I think the way the Social Security administration sets it up, the options are all pretty similar. We all have this personal belief that we’ll live longer than average (but not everyone can live longer than average, expect if you’re from Lake Wobegon, MN). And that makes us think we’re better off waiting, but it probably is all pretty equal.

I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

Today we celebrate Tax Day. Celebrate isn’t quite the best word, but let’s paint a happy face on this.

There a million things we can talk about with regard to

taxes and personal finance, but let’s focus on one of the big changes that hit

in 2018 that fundamentally affects a MAJOR financial decision we make—the

mortgage on your house.

The major tax overhaul that passed at the end of 2017 is

probably the biggest in my adult life.

It puts a few tried-and-true nuggets of tax wisdom on their head,

particularly how “itemized deductions” are treated, including your

mortgage. Let’s dive in and see how that

changes things.

Quick primer on how

taxes were

Remember, I’m

not an accountant, so this is my best understanding of how things were and

are.

Before, you as a tax payer had to decide to take the

standard deduction or itemize your deductions.

You can only do one or the other, so the general idea is to do whichever

is “greater”.

Standard

Deduction

2017

2018

Single

$6,350

$12,000

Married

$12,700

$24,000

When you take the standard deduction, as the name implies,

you just get to reduce your taxable income by a standard amount. In 2017, if you were a married couple, that

amount was $12,700.

The alternative is to itemize your deductions. Things can certainly get complicated, but for

most people your itemized deductions are your state income taxes, and if you

own your own home your property taxes and the interest on your mortgage. If those three items were more than $12,700

then it made sense to itemize your deductions.

In 2017, for the Fox family, our state taxes were about

$10,000, property taxes about $6,000, and interest on our mortgage about

$9,000. All that adds up to about $25,000. So, it made a lot of sense for us to itemize

our deductions. We got to reduce our

taxable income by $25k instead of $13k.

That probably saved us about $4,000 in taxes. Not bad.

Quick primer on what

changed for 2018

There were a ton of changes in the new tax law (I think the

actual document was well over 1000 pages—Yikes!!!). But let’s hit the highlights.

The same logic holds where as a taxpayer, you should pick

whichever is greater, itemizing your deductions or taking the standard

deduction. But that’s where some major

changes occurred.

First, you can see that the standard deductions nearly

doubled. That alone makes the number of

taxpayers who would take the standard deduction much higher than before.

Looking at our situation from 2017, we had $25,000 in

standard deductions while the standard deduction is $24,000. Back in 2017 it was a no-brainer, but in 2018

it became nearly a wash. But that’s just

the tip of the iceberg.

The second major change is that there is a limit of how much

you can deduct on your itemized deductions for state and property taxes. In 2017 there was no limit, so in our

situation we were able to deduct $16,000 ($10k for state taxes and $6k for

property taxes).

Now the limit is $10,000.

That’s a major game changer.

Using our 2017 numbers instead of deducting $16,000 for state and

property taxes, we hit the limit of $10,000.

Add the $9,000 for mortgage interest and we can only deduct $19,000. That is much less than the $24,000 standard

deduction, so with the new tax laws, we will

take the standard deduction.

Basically, for it to make sense for you to itemize your deductions,

you need to have over $14,000 of interest expense on your mortgage. Just using round numbers, if your interest

rate is 4% (and if it’s higher than that, you should refinance

?), that means you’d have a $350,000

mortgage. Anything less than that, and

you’re better off taking the standard deduction.

How this affects your

mortgage

Let’s bring this full circle, back to the headline of this

post—How does all this affect your mortgage?

If you boil it all down, basically you should take on debt

if the interest rate is really low.

However, the tax change “increases” your mortgage rate because it’s not

going to make sense to be able to deduct the interest.

Before if you had a 4% mortgage, after you deduct the

interest on that mortgage from your taxes, it might seem more like a 2.5% to 3%

rate. Obviously, that’s a big

difference. Maybe your internal

calculations look at a loan at 4% as high enough to pay off fast, but not one at

2.5%. Makes sense.

However, now most of us can’t deduct that mortgage interest.

Mortgage rates are

rising

For the past several years, we have been enjoying

historically low interest rates which have translated to historically low

mortgage rates. However, that has been

changing. A few years back a 30-year

mortgage might have been at 3.5% while now it is at 5%.

If you combine that impact with the tax deductibility, you

have a major impact. Before you had a

low rate that was tax deductible. Let’s

say it was a 3.5% rate that “felt” like 2.5% after you deducted the interest on

your taxes.

Now if you get a mortgage that rate will be 5%. That’s an enormous change, big enough to

fundamentally shift the decision of whether or not you should pay off your

mortgage faster.

Remember, that paying off a loan is basically making an

“risk-free” investment, similar to a bond.

Before, paying off your mortgage would give you a 2.5% guaranteed

return. That’s not great. For the Fox family, we looked at that as too

low. We’d rather take on more risk and

invest that money in the stock market.

Now with the changes, being able to get a 5% guaranteed

return changes our decision. We wouldn’t

do it at 2.5% but we would at 5%. This

becomes real because now Foxy Lady and I will start using extra cash we have to

pay off our mortgage faster.

This is a huge game changer that impacts millions of

Americans. It changed a central decision

we had to make for personal finance.

Maybe it will change that for you too.