“How can something so small be so impressive?” –Belinda Heggen

1% doesn’t seem like a lot. It’s the extra sales tax my city adds, hoping I don’t notice it. It’s the maximum amount of gross stuff food companies can put in packaged food without having to tell us (I don’t know it that’s true or not). But in investing 1%, while so easy to overlook, can make a huge difference. Here we’re going to find out how we can get that 1% to help us.

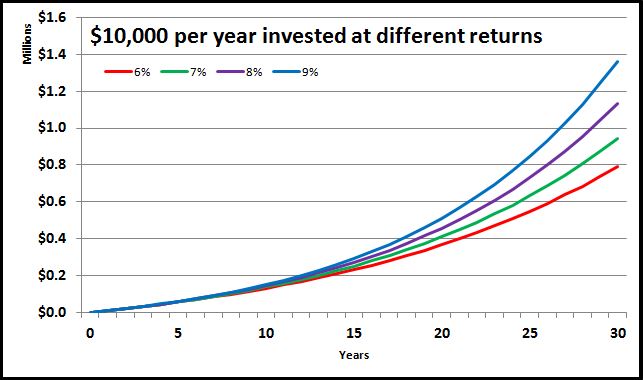

Let’s go back to my neighbors, Mr and Mrs Grizzly. Each year they will save $10,000, investing it in a stock index mutual fund with an expected annual return of 6%. After 30 years, they expect to have $790,581 saved (good time for the disclaimer that I am not predicting future stock performance, just giving an example), a tidy little sum to help see them through their golden years.

However, Mrs Grizzly starts playing with her spreadsheet and changes the annual return from 6% to 7% just to see what happens. She’s astounded to see that the $790,581 that she gets with a 6% return balloons to $944,608 if she assumes a 7% return; that increase in the annual return of 1% led to an increase in her nest egg of 19%. Tempting fate she sees what happens with an 8% return: $1,132,832. She’s a millionaire now. Cranking the return up to 9% made her nest egg $1,363,075; just increasing her return 3% nearly doubles how much she and Mr Grizzly will have to retire on. Ladies and gentlemen, welcome to the power of compound interest!!!

The point here is that a seemingly small 1% change in your investment return can make a huge difference over time. By tailoring your investment strategies to collect as many “1% coupons” as possible, you can substantially increase, even double, the value of your nest egg.

So how do we get those higher returns? Most people will default to higher stock returns: “It’s a no-brainer. Instead of investing in the stocks and mutual funds that return 6%, let’s invest in the ones that return 7%.” Unfortunately, after reading A Random Walk Down Wall Street we know this isn’t so easy. For any given level of risk, our investment return is probably going to be what it will be.

Now that changing the actual investment return is out, what are our options? Fortunately there are a lot of other things that affect our total return beyond just what our investments give us. We’ll dive into each one of these with its own blog post, but a few to think about at a high level are:

- Mutual fund management fees: Each year mutual funds charge between 0.05% all the way up to 1.50% or more for management fees. Going from high-cost mutual funds to low-cost funds can easily get us a 1% coupon.

- Financial planner fees: There are a lot of people out there who are more than willing to tell you how to invest your money for a small fee. Except that fee doesn’t tend to be all that small: about 1-2% of your total assets. Do-it-yourself investing can absolutely give you that 1% coupon, and the results you produce will probably be similar to those your investment adviser would.

- Being smart with taxes: You know Uncle Sam is going to take his cut. However, you can delay when he takes his share with IRAs, 401k’s, etc. This allows you to keep the money longer, and it allows to you be taxed on the money later in your life when you will probably be in a lower tax bracket. Being smart with your taxes can easily get you a 1% coupon.

- Take the “free money” offered to you: Many of us work for companies that match 401k contributions. Except they only give you the extra money if you invest in your 401k. So at least putting in up the minimum amount of get the match can absolutely give you one or two 1% coupons.

- Proper asset allocation: We all know that some of your investments should be in higher return, riskier investments like stocks and some should be in lower return, less risky investments like bonds. Properly assessing your portfolio to know how much you already have in less risky investments (especially things like pensions, Social Security, your home equity, etc.), can allow you to safely put more money in investments like stocks. Over the long term, this could easily increase your return each year and get you a 1% coupon.

- Fully investing: So many people I talk to have $10,000 or $20,000 or $50,000 in their checking account that they’re “just waiting to figure out what to do with it.” These are certainly Champagne problems, but they are also fertile ground to find 1% coupons. Just taking that money and putting it in a bond fund instead of a checking or money market account could easily give that extra 1% or more; investing in a stock fund will provide even greater returns over the long run.

Those are just a few examples of how you can squeeze an extra 1% or more from your investment returns. You’ll notice that none of those strategies include “outsmart Wall Street and pick the stocks that are going to do the best.” I’m not that smart; I wish I was because then the Fox family would own its own island in the Caribbean next to Johnny Depp’s island. These are all really simple strategies that anyone can do, and each of which takes less than a couple hours to set up, and can lead to hundreds of thousands of dollars over your investing lifetime. The Fox family has benefited by these little strategies probably to the tune of 4-5% extra return each year over what seems typical among your average American investor, and that has equated to hundreds of thousands of dollars.

So here’s the bottom line: As you read this blog, we’ll constantly be finding “extra 1% coupons” that you can redeem to increase your overall investment returns. As Mrs Grizzly showed, even one of those can add $150k to your nest egg. If you can gather two or three or even more, you can double your nest egg.

These days there are even some ETFs such as SCHB with an expense ratio as low as .04%.

I prefer ETFs because they contain the diversification mutual funds do but also more control over the tax hit in non-retirement accounts.

Multiple ETFs with similar low expense ratios for a variety of investing strategies can be found at:

etfdb.com compare/lowest I expenses ratio/

That’s a great point on ETFs. Maybe there is a post in the future on the pros/cons of ETFs versus mutual funds 🙂

Thanks for the comment.