I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

When I wrote my three ingredients post, a few of you commented that I was crazy to have so much of our portfolio in stocks and so little in bonds (less than 1% in bonds). Did I have a death wish or something? What if I told you that I think a ton of people are leaving gobs of money on the table because they are investing too conservatively? Tell me more, you say.

We know that you need to balance risk and return in our investments. This is most clearly done when we choose our mix of stocks (more risky, higher average returns) and bonds (less risky, lower average returns). As an investor gets older they want to shift their asset allocation towards less risky investments because their time horizon is shortening. We all agree with this. So where is this hidden pot of gold I’m talking about?

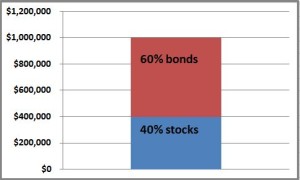

Let’s look at the example of Mr and Mrs Grizzly. They are both 65 years old and entering retirement. They worked hard over the years and socked away $1 million that will see them through their golden years. They do some internet research and learn that a sensible asset allocation in retirement is 40% stocks and 60% bonds, so they invest $400k in stocks and $600k in bonds. Knowing the long term average returns are 8% for stocks and 4% for bonds, they expect their $1 million nest egg to generate about $56,000 per year ($400k * 8% + $600k *4%) , knowing that some years it will be more and some years it will be less. So far so good, right?

THEY ARE LEAVING MAYBE $20,000 PER YEAR ON THE TABLE. That’s a ton of money. How can this be? They seem to be doing everything right. The answer is they are being way too conservative with their asset allocation. They shouldn’t be investing $600k in bonds and $400 in stocks; stocks should be a much higher percentage.

Waaaaiiiiiiiittttttttt!!! But didn’t we agree that about 60% of their portfolio should be in less risky investments? Yes, we did. Are you confused yet?

Hidden cash

Here’s what I didn’t tell you. Mr and Mrs Grizzly have other investments that act a lot like bonds that aren’t included in that $1 million. Both Mr Grizzly and Mrs Grizzly are eligible for Social Security with their monthly payments being $2000 each. If Mr Grizzly (age 65) went to a company like Fidelity and bought an annuity that paid him $2000 each month until he died (doesn’t that sound a lot like Social Security), that would cost about $450k. So in a way, Mr Grizzly’s Social Security payments are acting like a $450k government bond (theoretically it would be more than $450k since the US government has a better credit rating than Fidelity). And remember that Mrs Grizzly is getting similar payments, so as a couple they have about $900k worth of “bond-ish” investments.

Also, Mr and Mrs Grizzly own their home that they could probably sell for $300k. They don’t plan on selling but if they ever needed to they could tap the equity in their home either by selling it or doing a reverse mortgage. So in a way, their house is another savings account for $300k.

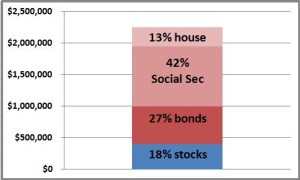

If you add that up, all the sudden the picture looks really different. They have about $950k of Social Security benefits that have the safety of a government bond. Plus they have that $300k equity in their house. That’s $1.25 million right there.

Investing your portfolio

So now let’s bring this bad boy full circle. Remember their $1 million nest egg they were looking to invest? Look at that in the context of their Social Security and house. Now their total “assets” are about $2.25 million. If you believe that the Social Security and house kind of feel like a bond, just those by themselves account for 55% of their portfolio. If on top of that if you invest 60% of their $1 million nest egg in bonds, they have over 80% of their money in bonds, and that seems way too high.

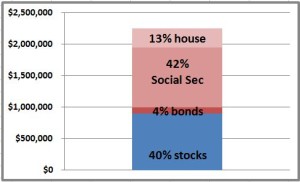

On the other hand, let’s say they only put $100k of their nest egg into bonds and the rest into stocks, after you include their social security and home, they’d be at about 60% bonds and 40% stocks. Isn’t that what they were aiming for the whole time?

Wow. It took a long time to get there, Stocky. The punchline better be worth it. Remember that with $600k in bonds and $400k in stocks, they had an expected return of about $56,000 per year. However, if they have $100k in bonds and $900k in stocks, because stocks are more volatile but have a higher expected return, they can expect about $76,000 ($800k * 8% + $100k *4%). THAT’S $20,000!!!

But aren’t they taking on a lot more risk to get that extra $20k? Remember, there’s no such thing as a free lunch. For sure, but if you look at it in the context of their Social Security benefits and their home, they have a fair amount of cushion from “safe investments” to see them through any rough patches in the stock market.

I wrote this post to show that people really need to take account all the financial resources they have. In the Grizzly’s case, it was their Social Security benefits and their home. Others of you may be getting a pension (Medtronic is generous enough to offer the Fox family one) or a second home or a dozen other things like that.

When you take those cash flows into account, all the sudden it seems a lot more reasonable to invest the rest of your money a little more heavily in stocks which you know over the long haul will give you a better return.

I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

SPOILERS WARNING

Between the gore and the incest, there are some valuable personal finances lessons from A Game of Thrones. This Top 5 list is dedicated to all those who fell fighting for the living against the Night King.

5. Debt creeps up on

you: King Robert’s reign was a

largely peaceful and prosperous one. Yet

like so many people, Robert overspent and went into debt. It wasn’t any one thing and at first he

really didn’t seem to notice. However,

before too long Robert was hamstrung by his debt, and it force him to make bad

choices—the terrible marriage to Cersei being forced upon him since the

Lannisters held most of his debt.

That marriage to Cersei: we all know how that turned out for

Robert. Oops.

4. Everyone likes to

look richer than they are: Rather

ironic based on #5, but by season 4 the Lannisters are broke. Their gold mines stopped producing and they

are deeply indebted to the Iron Bank.

Sounds pretty dire, but you wouldn’t know it by looking at

them. They are still “rich as a

Lannister” and give the outward appearance that they are rolling in the gold

dragons. In no way do they let that they

aren’t rich as ever, and why would they?

Who would want to show their rear end to others?

3. “How would we know

we can’t fly unless we leap from some tall tower”: Euron Greyjoy is one of the creepiest dudes

in the series, but I love this line.

Life is about taking on risk, understanding it, and making

decisions that give you the most upside for the risk you take. This is especially true with investing.

The key is taking smart “leaps,” those where the rewards

more than offset the risks. Stocks

definitely fall into that category.

2. “Power resides

where people think it resides”: Here

Varys speaks one of the most important lines in the entire series.

There’s probably no statement that describes our financial

system better. Banks work because people

have think they work—you put your money in and you get it out. Fiat currency is really just paper with

colored ink, but they work because people think they can reliably use those

pieces of paper to get other stuff.

The best, most recent example has been Bitcoin. For a while people thought Bitcoin was really

valuable so it went up to $19,000 (Dec 2017).

Then all the sudden people didn’t think it was valuable so it plunged

down to $3200 (Dec 2018), and now it’s back up to $5300. Nothing has really changed about its value or

intrinsic net worth except what people think

about its value.

1. Being good at personal finance opens up A

LOT of opportunities: Littlefinger

was my absolute favorite character, and he’s a great example of the power that

comes with being really good with personal finances.

He started out as a nobody and rose to arguably the most

important and richest person in the seven kingdoms. How did he do it? Investing well and being good with

money. He “had a gift for rubbing two

golden dragons together and breeding a third.”

In our world financial literacy is abysmal. Those who can master those skills can do

quite well; the average salary for a financial planner is over

$100,000. Smart financial decisions

can make a millionaire out of nearly anyone.

As Littlefinger shows, the sky’s the limit with this skillset.

A few years back, I wrote a blog comparing the financials of renting versus buying your house. Back then renting came out ahead when you just looked at the dollars, which was a bit surprising. It seemed to buck conventional wisdom that buying is also the best option.

This seems especially important in light of some of the tax changes that impact your mortgage and property tax deductibility.

For this post, I want to look at the choice from a purely financial perspective. And what better way to do that than break it down Dr Jack style? Just to put a little meat on the analytical bone, let’s assume we have a home that we could buy for $400,000 or we could rent for $2000 (I did a quick search on Zillow in a few different markets and this seemed reasonable).

UP-FRONT COSTS: When you rent, you have to give a deposit which is typically something like one month of rent, so that’s $2000. Not a big deal in the grand scheme of things. When you buy, your down payment is in the range of 20% (or maybe even higher since the 2008 financial crisis—the Fox family had to put 25% down on our house). That would mean $80,000 if you’re buying.

At first glance that may not seem like a big deal because it’s still your money, it just happens to be “invested” (did you notice how I used quotes there?) in your home. However, when your $80,000 is tied up in your house you can’t invest it (no quotes there) in the stock market. Since the stock market historically returns about 6% that means you’re passing up $4800 per year on average. Over an investing career that ends up being a TON of money.

Advantage: Bid advantage to RENTING

RISING INTEREST RATES: We’ve been living the last decade with historically low interest rates. A 30-year fixed loan was in the 3.5% range, and all was well. Since then interest rates have steadily crept up.

The math on interest rate increases is pretty powerful. A 1% increase would increase your monthly mortgage payment about $3200 per year or about $280 per month.

A couple months ago, interest rates rose to about 5%, but since then it has settled down to about 4%. Either way, interest rates are going up, and it seems that will probably be the long-term trend.

Advantage: RENTING

MONTHLY PAYMENT: The most common knock I hear on renting is “every month you pay rent, you’re throwing that money away.” I hate that comment, and part of this post is to show how little sense that makes. Obviously when you are renting, your monthly payment is your rent, $2000 in this example.

When you buy, your monthly payment is your mortgage (here we aren’t going to include insurance and taxes, that will come later). If you have a typical 30-year mortgage, let’s say at 4.5% interest, your payment is going to be about $1620 per month. That’s quite a bit less than you’re paying in rent, so obviously that’s an advantage for buying, but then there’s another little bit of good news. That $1620 you’re paying is mostly interest, but a small amount is going towards paying down your loan. In a way that can be seen as you “saving” money. In this example the amount going towards you’re loan would be about $200 per month. So that’s pretty nice. Of course that “forced savings” has a low return compared to the stock market, so it’s not as good as it could be.

Of course, that means that about $1400 per month is going to interest. So when people say that you’re throwing away your rent, can’t you say the same thing for the interest on your mortgage? Either way, this is definitely an advantage to buying.

Advantage: BUYING

OTHER COSTS: With renting, once you pay that rent check, you’re pretty much done. With buying you have a lot of other expenses that nickel-and-dime you to death. Property taxes have to be paid (let’s say 1% of the property value so that’s $333 per month). If you live in a condo complex or an association you might have monthly dues that could range from pretty minor to a significant chunk of money (when the Foxes lived in a condo in downtown Chicago, our monthly association fees were $900 per month—ouch!!!). Those can definitely add up, so that’s a nice advantage to renting.

Advantage: RENTING

TAX ADVANTAGES: This is where a huge change has happened recently. Before, all your mortgage interest and property taxes were tax deductible. Now there is a $10,000 limit on those deductions. In a lot of scenarios, your property taxes won’t be tax deductible. Because of the higher standard deduction, a lot of times it won’t make sense to deduct your mortgage interest either.

Before, the deduction for your mortgage interest and property taxes might be worth about $600 per month. Now that is certainly less, maybe all the way down to nothing.

Advantage: WASH

INFLATION: Once you buy your house your biggest cost, your mortgage, is going to stay put. We’ve talked about inflation before, and the enormous impact that even a little inflation can have on expenses after many years, so this seems pretty awesome that you don’t need to worry about it for your biggest expense.

With rent “that’s where they get you”. Rents almost always go up. Often there are laws that put a cap on how much they can go up, 2% seems a number I’ve heard before, so that provides some relief, but even that 2% can be a big deal. If today your rent is $2000, in 10 years it would be $2440, in 20 years it would be $2970, and in 50 years it would be $5390. That sucks, especially when compared to buying where your mortgage payment will always stay the same.

Advantage: Big advantage to BUYING

SELF-DETERMINATION: A neighbor was renting a few houses down from us. The family loved the house, loved the neighborhood, loved the neighbors (of course they did). But one day the landlord called her and said she wasn’t renewing the lease because she (the landlord) was moving into the house. That family that was renting was FORCED to move even though they didn’t want to. That sucks.

When you rent, you’re definitely at the whim of your landlord. If you buy, you are in control of your own destiny, baby. Get drunk off that power.

Advantage: BUYING

UPKEEP: One of the super-nice things about renting is that you don’t need to worry about when things break down. If there is a problem with the toilet, call the landlord. Water damage from the really bad storm, call the landlord. Fridge on the fritz, whatever—call the landlord. In general this is an awesome advantage. This is even better if you’re not a very handy person.

If you own a home, whenever anything goes wrong you need to fix it yourself (hence my “handy” comment) or worse you have to pay someone to fix it for you. There’s no perfect estimate, but a generally accepted rule is you should plan on spending 1% of the home’s value on maintenance. In our example that would be about $4000 per year.

Advantage: RENTING

NICENESS: As an owner, if you want to make your place nicer you absolutely can. If you want a pool, build it; hardwood floors, install them; custom closets, wallpaper, nice landscaping, and on and on. As a renter there’s a reluctance to do it because in some sense you’re paying to make someone else’s property nicer. If you rent there for years and years, maybe that’s not a huge deal, but that “self-determination” issue rears its ugly head.

I don’t have statistics on this, but I bet that most renters would love to make their place nicer, but just don’t because there is some deep attitude that you don’t do that when you rent. I totally get it and understand it, but it sucks that this keeps you from making your place as nice as it would otherwise be.

Advantage: BUYING

WORST-CASE SCENARIO: I’m not talking about your hot-water heater going bad or having to replace the roof (those we captured in “Upkeep”). Here I’m talking about real worst case scenarios like a natural disaster (in California earthquakes aren’t covered by most homeowners insurance policies; you can get earthquake insurance which is really expensive, so most don’t get it), or the neighborhood really turns bad, or termites or black mold infestations happen inside the walls. Let your imagination run with this for a second and you can really think of some nasty stuff.

As a renter, you can pick up and leave the nightmare behind. Just go somewhere else and start paying someone else rent, and problem solved. Not so if you own the home. Your single largest investment is at risk. Sucks to be you.

By its nature, the worst-case scenario isn’t very likely, but still it could happen. This is one of the things that keeps me up at night as a homeowner.

Advantage: RENTING

ASSET ALLOCATION: A mortgage is a “forced savings” program in a way. Every month you’re making a mortgage payment and part of that goes towards your equity that you can use as you get older (reverse mortgages, cash-out refinances) or pass on to your heirs. After 30 years your house will probably be paid off and you’ll have a tidy little sum of cash to supplement your portfolio. Also, because home values tend to be much steadier than stocks, in a way this investment might seem like a bond.

We saw how crazy important asset allocation is, so if you have a lot of home equity, that might make you feel more comfortable to put a bigger portion of your portfolio into stocks which historically have a higher return. This is a bit of a tricky one, but there’s definitely some level of advantage there.

Advantage: WASH

REALTOR COSTS: There will come a time when you are ready to leave your current home and move somewhere else. If you’re renting this is easy (but not super-easy). Usually, you’ll wait for your lease to expire and then head on down the road. If you need to move right away and your lease isn’t up for a while, that can create a bit of a challenge of breaking you’re lease. That could be as easy as paying a penalty of a month’s rent, or your landlord could play hardball and hold you to your lease until the end. So this can be a pain, but more in the “moderate” zone.

When you own a home and have to sell it, that is a monumental undertaking. Getting a home ready for sale, listing it, showing it, and ultimately closing the sale can take months from beginning to end. Also, it’s not cheap. While realtor fees vary, they average about 6% of the home’s value. In our little example that would be $24,000. That is a lot of money. If you’ve been in the house for 30 years, that will amortize to less than $1000 per year, but if you’ve only been living there a few years that could be thousands of dollars per year that you need to tack on the to “Buy” expense column.

Advantage: Big advantage to RENTING

PRICE APPRECIATION: We saved the best for last, kind of. When you own your home, you get to take advantage of any price increases that your home experiences. Of course, if your home goes down in value, you suffer those loses too. However, like stocks, homes have historically increased in value over time, with notable exceptions like when home values crashed in 2008.

That’s great news, right? No question. However, it’s not as good as most people think. You hear all sorts of crazy stories about people making a killing off their house, but those tend to be anecdotes rather than the rule. The numbers are hard to come by but I think the most definitive and well-respected data, the Case-Shiller index (developed by my BFF Robert Schiller) shows that prices for existing homes have only increased 0.5% over the past 40 years after you account for inflation.

THAT’S CRAZY. That goes against everything we hear. How can that be? Well his index controls for things like home sizes getting bigger, houses getting nicer features, etc. So it really tries to do an apple-to-apples comparison of what you can expect will happen to your home. So home prices do tend upward, but just not at anywhere near the pace that we’ve come to believe.

Advantage: BUYING

Buy

Rent

Investment return on down payment

$400

Interest/rent

$1,333

$2,000

Property taxes

$333

Tax advantage

$0

Maintenance

$333

Realtor fees (5 years)

$400

TOTAL

$2,800

$2,000

If you put it all together Buying “loses” with a score of 5-6-2. Furthermore the math shows that Renting comes out ahead on a monthly expense basis, and it has become an even bigger advantage with the new tax laws. Yet, Buying wins on a lot of those intangibles. Ahhhh, this is why the decision is so complex. Hopefully you saw my point that buying isn’t the unambiguously better option.

If you look at the numbers, it really breaks down to two major factors—realtor costs and price appreciation. The longer you’re in your home, the more years you can spread that 6% realty fee over. So if you’re planning on moving after a few years, that becomes a major disadvantage to buying. Your home appreciating in the icing on the cake that can really make the whole difference. However, the Case-Schiller index showed that prices don’t rise nearly as fast as everyone seems to think (hence, I didn’t even include it in the expense comparison).

It’s a tough call, but the dollars are real. Renting costs about $800 less than Buying in our example; that 40%!!!

The Fox family owns our home, and it has turned out to be the best investment we’ve ever made. We bought in 2010 when the housing market in Southern California had been thoroughly thrashed by the 2008 crisis. In the past 5 years our home has rebounded, more than doubling in value. We would have missed all that had we rented, but if I’m honest with myself, it was just really lucky timing. Sometimes it’s better to be lucky that good.

Long before there were ever stocks or bonds, the original investment was gold. Heck, even before there was paper currency or even coins, gold was the original “money”.

That begs the question, What

role should gold have in your portfolio?

If you don’t want to read to the end, my quick answer is “None”. However, if you want to have a bit of a

better answer, let’s dig in.

Gold as an investment

Just like stocks and bonds, gold is an investment. The idea is to buy it and have it increase in value. Makes sense. And historically, it seems to have been a good one—back in 1950 an ounce of gold was worth about $375 and today it’s worth about $1300. Not bad (or is it???).

However, there is a major difference between gold (and broadly commodities) as an investment compared to stocks and bonds. Gold is a store of value. If you buy gold it doesn’t “do” anything. It just sits in a vault collecting dust until you sell it to someone else.

That’s very different from stocks and bonds. When you buy a stock that money “does” something. It builds a factory that produces stuff or it buys a car that delivers goods or on and on. What ever it is, it’s creating something of value, making the pie bigger. That is a huge difference compared to gold, and it’s a huge advantage that stocks and bonds have over gold. You actually see that play out by looking at the long-term investment performance of gold versus stocks.

Golden diversification

Statistically speaking, gold gives an investor more diversification than probably any other asset. We all know that diversification is a good thing, so this means that gold is a great investment, right?

Well, not really.

Stick with me on this one. Gold

is negatively correlated with

stocks (for you fellow statistics nerds, the correlation is about -0.12). Basically, that means when stocks go up gold

tends to go down, and when stocks go down gold tends to go up.

Over the short term, that’s probably a pretty good thing, especially if you want to make sure that your investments don’t tank. In fact, that’s one of the reasons gold is sometimes called “portfolio insurance”. It helps protect the value of your portfolio if stocks start falling, since gold tends to go up when stocks go down.

However, over the long-term, that’s super

counter-productive. We all know that

over longer periods of time, stocks have a

very strong upward trend. If gold is

negatively correlated with stocks, and if over the long-term stocks nearly

always go up, then that means that over the long-term gold nearly always goes

(wait for it) . . . down.

That doesn’t seem right, but the data is solid. Look back to 1950: an ounce of gold cost

$375. About 70 years later, in 2019,

it’s about $1300. That’s an increase of

about 250% which might seem pretty good, but over 70 years that’s actually

pretty bad, about 1.8% per year.

Contrast that with stocks.

Back in 1950 the S&P 500 started at 17, and today it’s at about

2900. That’s an increase of about

17,000%, or about 7.7% per year. WOW!!!

Just to add salt in the wound, inflation (it pains me to say

since I think the data

is suspect) was about 3.5% since 1950.

Put all that together, and gold has actually lost purchasing power since

1950. Yikes!!!

A matter of faith

Fundamentally, if you have faith that the world will continue to operate with some sense of order, then gold isn’t a very good investment. So long as people accept those green pieces of paper you call dollars in exchange for goods and services and our laws continue to work, gold is just a shiny yellow metal.

However, if society unravels, then gold becomes the universal currency. The 1930s (Great Depression), the 1970s (OPEC shock), and 2008 (Great Recession) were all periods where gold experienced huge price increases. Those are also when the viability of the financial world order were in question. Each time, people were actively questioning if capitalism and banks and the general financial ecosystem worked.

People got all worked up and thought we were on the brink of oblivion. Gold became a “safe haven”. People knew no matter what happened, that shiny yellow metal would be worth something. They didn’t necessarily believe that about pieces of paper called dollars, euros, and yuans.

Yet, the world order hasn’t crumbled. Fiat currencies are still worth

something. Laws still work, so that

stock you own means that 1/1,000,000 of that factory and all it’s input belongs

to you. Hence, gold remains just a shiny,

yellow metal.

The bottom line is that stocks have been a great long-term

investment, and gold hasn’t. And that’s

directly tied to the world maintaining a sense of order. So long as you think that world order is

durable and we’re not going to descend into anarchy Walking-Dead style, then gold isn’t going to be a good investment.

So the survey says: “Stay away from gold as an investment in

your portfolio.”

In the United States, Social Security is an important part of most peoples’ retirements, actually probably too important in many instances. Social Security is a fairly simple program that was designed to be pretty idiot-proof. You don’t really need to make many decisions for it, which contrasts sharply with all the decisions you need to make on your other investments (like tax strategies, asset allocation, picking investments, etc.).

With Social Security, you just work and the government takes its 12.4% (6.2% from you and 6.2% from your employer) of your compensation. In fact, you don’t really have a choice in the matter and the government does it automatically. Then when you get old, the government gives you a monthly pension. Not real complicated on your end.

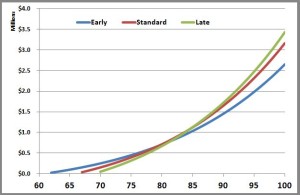

However, there is one really important decision you need to make regarding Social Security: when you start taking it. Basically, you have three options: 1) Early retirement-when you turn 62; 2) Regular retirement-when you turn 67 for most of us; 3) Late retirement-when you turn 70. And as you would expect, if you start taking Social Security later, you get a larger monthly check from the government.

This is obviously an important choice to make, and it’s one that gets a lot of press coverage with all sorts of people opining on what to do (I guess with this post, I am adding my opines to those ranks). Generally speaking, the advice slants towards taking it later. Yet, I wonder if that’s really good advice. Using my handy-dandy computer, let’s go to the numbers to see what they tell us.

I checked my Social Security statement and I’ll be able to pick from one of the three choices:

Age to start taking Social Security

Monthly check

Early retirement—age 62

$1800

Full retirement—age 67

$2600

Delayed retirement—age 70

$3200

As you would expect, the answer to this riddle is a morbid one. When do you expect to die? The longer you live, the more it makes sense to delay taking Social Security so you can get the bigger check. That’s not a tremendous insight, but when you do the math, you start to see some interesting things going on. I fully appreciate that Social Security is very nuanced and complex, so I am just covering the simple basics here.

In my analysis to be able to compare the different scenarios, I assumed that I saved all the Social Security checks and was able to invest them at 4%, about the historic rate for a bond. If you do that the table above expands to this:

Age to start taking Social Security

Monthly check

Highest value

Early retirement—age 62

$1800

Die before age 79

Full retirement—age 67

$2600

Die between age 80 and 84

Delayed retirement—age 70

$3200

Die after age 85

That’s pretty profound actually. The average life expectancy in the United States is 76 for men and 81 for women. Doesn’t that mean that most of us should be taking Social Security with the early option? That contradicts most of the advice out there on this topic. That, ladies and gentlemen, is why Stocky is here for you. This is where it starts to get fun, and we can apply a little game theory (awesome!!!).

When to start Social Security?

Actually, once you reach age 62, the life expectancy of those still alive (and able to make the decision on Social Security) is 82 for men and 85 for women. This makes sense because you’ve survived to 62 so by definition you didn’t die before then (awesome insight, Stocky), and those early deaths pull down that initial life expectancy model.

Since women are better than men as a general rule (Foxy Lady took over typing for just a second there), let’s look at this decision as a 62 year-old-woman. She needs to make a decision on when to take Social Security. She knows her life expectancy at this point is 85, which means there’s about a 50% chance she makes it to 85. So the worst choice for a 62 year-old is to take the early retirement option. She’s probably going to live long enough that either full retirement or delayed retirement is the better option.

At 62 she does the smart thing, and decides to wait. Her next decision comes at age 67, assuming she lives that long (there’s about a 5% chance she’ll die during those five years). But a similar thing happens—when she was 62 her life expectancy was 85 (right on the border of picking between full retirement and delayed retirement), but now that she’s 67 her life expectancy jumps up a year to 86. So if she makes it to 67 then she’s better off taking the delayed retirement (of course, there’s about a 4% chance she’ll die before she makes it to 70).

That’s a little bit weird though, isn’t it? It kind of feels like you’re that horse with a carrot dangling over his head, keeping him walking forward. It’s a bit of a conundrum. At any given time, you’re better off delaying starting your Social Security, so the math tells you to keep waiting and waiting. But if the dice come up snake eyes and you die, then you miss out on everything (not strictly true, but true enough for our analysis).

And keep in mind that since Foxy Lady hijacked Stocky’s computer, we’ve done this analysis for women. The math tells you that it’s just about a wash between taking Social Security at 67 or 70. Since women live on average 3 years longer, for men you would think it means that the advantage leans towards taking it early.

What does it really matter?

So the analysis tells us that we’re better off waiting if you’re a woman and it’s really close if you’re a man. And of course the longer we wait, the further we come out ahead by taking delayed retirement instead of early or full retirement. But how big of numbers are we talking?

Remember, the cut off for when full retirement becomes better is at about 80 years old. The cut off for when delayed retirement becomes better is about 85 years old.

Future value of Social Security payments

Age

Early retirement (62)

Full retirement (67)

Delayed retirement (70)

85

$1,031,256

$1,119,603

$1,125,233

90

$1,450,231

$1,644,630

$1,716,663

100

$2,647,751

$3,158,200

$3,431,844

Those are meaningful differences. If you make it to 100 years old, delayed retirement comes out about $800,000 higher than early retirement. However, those are in future dollars, 38 years into the future if you’re 62 today and faced with this decision. That $800,000 when you’re 100 would be worth about $370,000 today. Of course that’s if you make it to 100, which isn’t really likely (about a 3% chance).

If you make it to 90 years old (you have less than a 30% chance) then the difference is about $260,000 in future dollars which is about $150,000 today.

Wrapping up, I’m really torn on this. There’s a little bit of a prisoner’s dilemma type thing working that keeps making you want to push back when you start collecting. And then when you look at the upside of delaying retirement, the numbers are pretty big (whenever you’re talking about hundreds of thousands of dollars, that’s real money), but the chances of us making it to that super-golden age are pretty small.

I suppose it’s best to wait, but I’m giving that a pretty “luke-warm” endorsement. It certainly isn’t the “slam dunk” that so many pundits make it out to be.

Actually, I think the way the Social Security administration sets it up, the options are all pretty similar. We all have this personal belief that we’ll live longer than average (but not everyone can live longer than average, expect if you’re from Lake Wobegon, MN). And that makes us think we’re better off waiting, but it probably is all pretty equal.

A few weeks ago we talked about mutual fund fees. There’s a big range, and one of the ways I win when investing is by minimizing the fee that I pay. It begs the question: How low can mutual fund fees go?

Quick historical perspective

Mutual funds have been around for a long time, dating back

to 1924 with Massachusetts Investors Trust.

Back then they had a management team that actively picked which stocks

to invest in, very similar to the actively managed mutual funds of today. Just like today, those mutual fund managers

were paid handsomely.

In 1976 Vanguard started the first index mutual fund based

on the S&P 500. Just like today, the

index mutual fund had costs significantly lower than its actively managed

peers. At first, the index idea didn’t

catch on, but over the next 40 years it became the dominant investment vehicle

for ordinary foxes.

Race to the bottom

for fees

Because index mutual funds are a bit of a commodity, the real differentiator is management fees. I started investing in 1996 and I remember that my S&P 500 had a management fee of 0.30%. At the time that seemed super low. Today, that same mutual fund has a management fee of 0.14%, and if you get their Admiral Shares (at least $10,000 invested) the fee goes down to 0.04%. DEFLATION!!!

Of course, that begs the question, how low could management

fees go? Fidelity answered that this

summer when they launched a line of index mutual funds with a management fee of

0.00%–NO FEE!!!

There’s no such thing as a free lunch, so why would Fidelity

do this? It seems like a simple

marketing ploy of having a loss leader. They’ll lose a little bit on these mutual

funds to get customers with the hopes that they get other products/services

from Fidelity.

How big a deal is

this?

Obviously getting something for free is better than paying

for it. Let’s figure out how big a deal

this really is.

As we just said, Vanguard offers a US index mutual fund with a 0.04% fee. International funds are a bit more expensive to manage and Vanguard’s is at 0.11%. If you’re diversified as I have suggested in our Three Ingredients post, let’s assume your average management fee is 0.08%.

So how much are you saving by going with Fidelity’s zero-fee

mutual funds over Vanguard’s index funds?

If you had a million dollar portfolio, that would come to about $800 per

year. That’s not a ton of money, but

it’s enough for Foxy Lady and I to go out to dinner once a month, so that’s

kinda nice.

But the real value comes in when that money compounds over

time. Over an investing lifetime that

little bit would add up to about $41k.

Again, that may not seem like a lot, but it’s about as much as the

average American has saved, so maybe it is a lot.

For us, I think we’ve been with Vanguard so long that it

would be hard to convert over to Fidelity’s zero-fee funds. There’s the tax implications of selling the

funds and paying capital gains which would be a lot. Plus, there’s the inconvenience of resetting

everything up again. Finally, there’s the

risk that I would get caught out of the market while my money was being

transferred.

The first reason (the taxes) is probably the real

reason. $800 per year pays for a lot of

hassle. However, if I was advising

someone just starting out who hadn’t already chosen Vanguard, I think this

would certainly tip the scales in Fidelity’s favor—I would recommend they go

with Fidelity and those zero-fee funds.

Either way, the point is that management fees are really

going to the basement and then lower.

That’s a real boon for investors.

“If you have to ask how much it costs, you can’t afford it.”—JP Morgan

Imagine that you’re going to buy something that costs over $1000, maybe a flat-screen TV or a new set of tires for your car. At some point during your decision-making process would you ask how much what you were getting costs? Of course you would. Unless you’re JP Morgan, a normal person figures out what something costs before he or she buys it.

Yet that is exactly what happens when people invest their money in mutual funds; they have no idea how much they are paying the mutual fund company to invest their money. I guarantee you ask 100 people who have 401k accounts how much they paid in management fees last year, and less than 5 will know, and those 5 would probably just get lucky. Even humble Mr Fox couldn’t tell you how much I pay Vanguard each year in management fees(important statement so I had to revert to third person), and I’m obsessed with this stuff.

And the crazy thing is with investing there are so many unknowns and random events, namely how your investments are going to do in the future, but one of the things we can control, how much we spend on mutual fund management fees, receives so little focus and attention.

Why are

management fees swept under the rug?

First, investment companies have every incentive to hide the fact that these even exist. Obviously,if Vanguard or Fidelity or American Funds can convince naïve investors that there’s no charge for investing their money, they’re more likely to do it—that’s economics 101. SEC rules require that funds publish their management fees, yet they tend to be in the smaller print, much less conspicuous than the proclamation that “Our fund has beaten its comparable benchmark 7 of the last 10 years, before fees.”

Second, the amounts tend to seem small. An actively-managed mutual fund with really high fees could be in the 1.5% range while a really large index mutual fund might bottom out at less than 0.1%. That spread of 1.4% from high to low may not seem like a lot on its surface, but that’s a 15x range. Also, due to the magic of compounding, over time, those fees would really add up. That difference in management fees could lead to a 13% difference in a person’s nest egg; that’s the difference between someone with high expenses having $500,000 in their 401k after a 30 year career and $565,000. That’s real money!!!

What are

the key determinants in how much a mutual fund charges for fees?

The single biggest factor in how much a mutual fund charges in management fees is whether it is a passively managed index fund or an actively managed fund. Index mutual funds don’t require much oversight. They find the index they want to mimic, like the S&P 500, then they have a computer program that monitors the fund’s holdings and makes small course-correction trades to ensure that the composition of the fund is as close to the index as possible. You have a couple people make sure the computer doesn’t go crazy and you’re set. There are still costs like accounting,marketing, keeping the website up, sending out account statements, etc., but it’s a pretty lean operation.

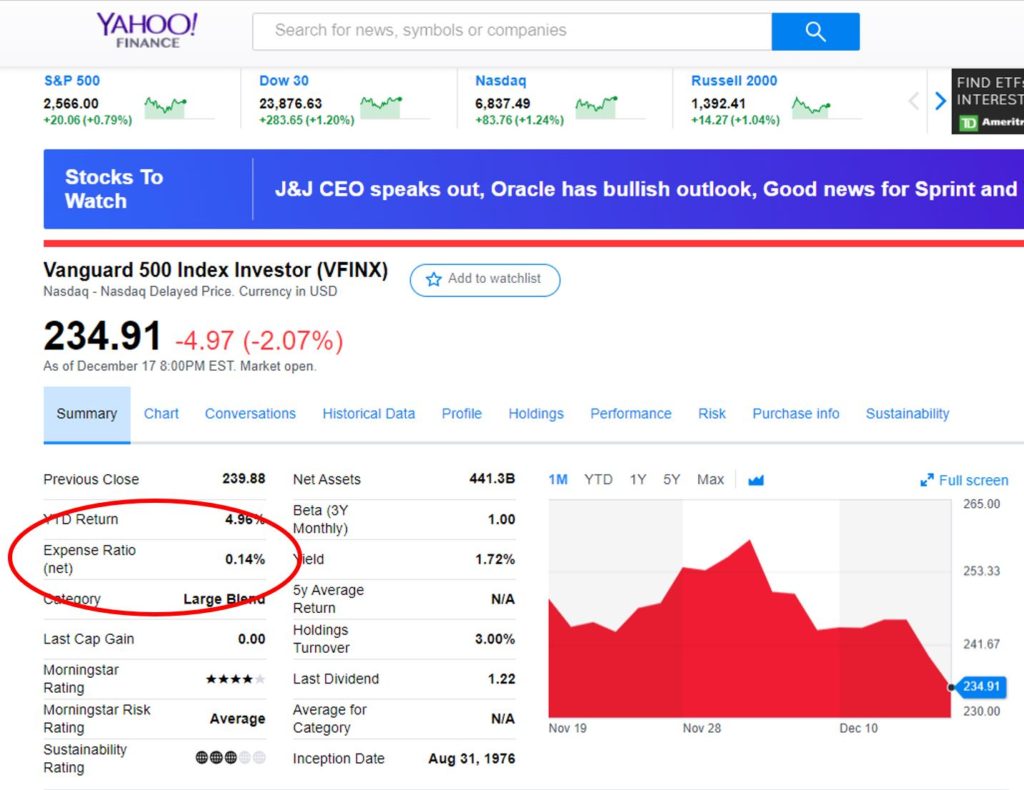

Also, with index mutual funds, in many ways they’re a commodity. Any S&P 500 index fund performs 99.99% identically to any other; that’s the very essence of an index mutual fund. So if there is no difference in the product, then companies must differentiate on cost. Not surprisingly, what is largely considered the best S&P 500 index fund (if you count it in terms of amount invested)is the one with the lowest costs: the Vanguard S&P 500 Index (VFINX).

Now on the complete other end of the expense spectrum you have the exorbitant fees associated with actively-managed mutual funds. There are mutual fund managers who get six-,seven-, and sometimes even eight-figure compensation packages. What justifies such astronomical pay? Just like free-agents in baseball these fund managers who are perceived as the best can go to the highest bidder, becoming celebrities in their own right (see: Lynch, Peter).

Beyond the compensation for the fund managers, these funds have a lot of costs. There are all sorts of industry and trade conferences that fund managers go to. And if you think they fly coach and stay at a Holiday Inn, I have a bridge to sell you. They work in glass palaces in downtown Boston and New York. Let me just say I once went into Fidelity’s headquarters in Boston and to quote a line from one of my favorite investing movies, Barbarians at the Gates, “it makes Buckingham Palace look like a Burger King.” Many offer gourmet lunches to their staffs every day, limos, in-house massage therapists, and the list goes on, but you get the point. And where does all this money come from? It comes from the extra 1.4% difference in management fees between an actively managed fund and an index fund.

Where can you find

the information?

This fancy thing called the internet actually makes this pretty easy to look at. Pretty much every finance website (Google,Yahoo!,etc.) lists every mutual fund’s expense ratio. This allows comparison shopping to be really easy. In about 5 minutes you could look up and compare the management fees of any of the mutual funds you are considering.

You can see the expense ratio circled in red on the left.

That’s not to say this is the only factor you should consider when choosing a mutual fund. That’s some deep water which would be a great topic for another post,but it is a really important one. Some would even argue that it is the single most important factor. Sadly it’s one that very, very few people are knowledgeable of. As you look to build your nest egg, it’s something you should absolutely know when you start making your investment decisions.

For our money, the Fox family is a believer in index mutual funds. In fact, 100% of all our money is in index mutual funds, so this is no joke to us. The management fee varies for each fund,management fees for US funds tend to be a little higher than international funds, but the range is about 0.05% to 0.20%, with the average coming in around 0.08%. So we are paying 0.08% of our total nestegg each year in management fees.

That’s what I do, but that doesn’t mean you have to do the same. There are many vocal proponents of actively managed mutual funds (by buddy Mike from Boston). Their points become especially compelling at times like this when the market is going down.

Believe what you will, but if what ever type of mutual fund you invest in you should always know what you are paying. After all, you aren’t JP Morgan. If you are paying a high management fee, just make sure you are getting your money’s worth.

A few years ago, I wrote about our worst investment of all time—commodities.

I think this is a classic case of deviating from the tried and true rules that you only need three investments in an effort to get creative and get higher returns. In general you should always resist that siren song. It cost us well over $100,000; that’s an expensive lesson.

After a few years of crapping performance, I finally bit the bullet, admitted defeat, took a huge loss, and sold my commodities.

Examining the wreckage

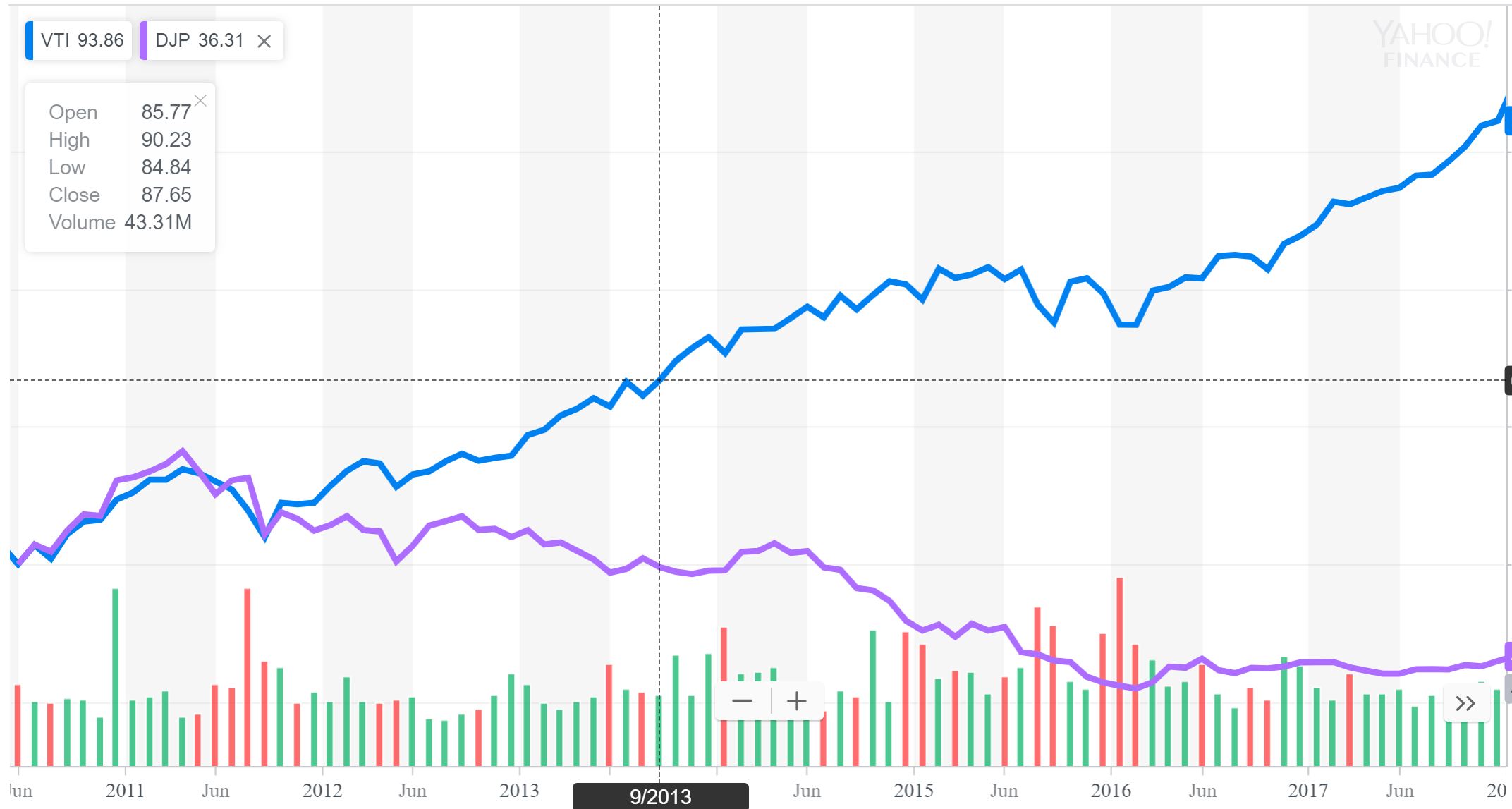

We starting buying commodities ETFs (ticker symbol DJP) in 2010 in small increments, and continued that through the end of 2014. When all was said and done, we had invested a total of about $100,000. By the time we sold, those ETFs were worth about $65,000, so we lost $35,000. Ouch!!!

But that’s only a small part of the loss. I knew, I KNEW, that we should invest that money in stocks but we didn’t. Had we invested that money in a stock index fund that $100,000 would have grown to nearly $200,000 by the end of 2017. I just threw up in my mouth.

A picture says a thousand words–the purple line is commodities for the period we owned them; the blue line is US stocks. OUCH!!!

This is a boneheaded mistake for the ages. Of course, as in most things in life, when you realize you made a mistake like that you need to move on. With stocks that’s tough psychologically to do because not only is it admitting failure, but it’s also locking in those losses. So long as you keep the investment you can always tell yourself there’s a chance that things will turn around.

Finally at the end of 2017, to take advantage of a little tax loss harvesting, I sold all our commodities investments. That horrendous chapter of our investing history was over.

Investing gods decide to humble me further

What unfolded was a story similar to one of those stories from the Bible where God continues to test someone’s faith. I sold all our commodities investments and invested them in US stock investments.

By the end of April 2018 commodities were up about 2% for the year while stocks were down 2%. ARE YOU KIDDING ME? After 7 years of stocks drastically outperforming commodities, the trend reversed right after I sold out my commodities. As you might guess, I was feeling picked on by some power beyond my understanding.

I kept to my guns and my faith was rewarded. By the end of August 2018, stocks had a big rally (up 8% for the year) while commodities were crushed (down 7% for the year). When all is said and done, stocks are up about 2% while commodities are down 5%. That difference equates to about $4000 in my favor.

There are a couple things I took away from this:

First, as an investor, you have to focus on the present and future, and not cling to the past. Second, sometimes your investments work out and sometimes they don’t, and you can’t get paralyzed by your investing failures. Third, exotic investments generally don’t work out over time.

All these really combine to illustrate all the things I did wrong with commodities. I should have just stuck to investing in stocks as I always preach on this blog. Once it started going bad, I should have cut and run instead of clinging to something in the hope that it would “come around.”

Better late than never. While I definitely left over $100,000 on the table, at least I didn’t leave that last $4000. That’s what I tell myself anyway.

My neighbor’s son, Rhino, just got engaged (I dubbed him rhino because the rhinoceros beetle is the strongest animal in the world pound-for-pound, and this kid is really strong). We’ve gotten to Rhino over the years. He was Mini and ‘Lil Fox’s first babysitter when we moved into the neighborhood, so of course he has a special place in our hearts.

We were talking about his engagement, starting out life, and obviously since it’s a conversation with me, how to do the right things financially.

It got me to thinking about what are the most important things to do in the world of personal finance when you are just getting started. For the soon-to-be newlyweds, here is my Top 5 list:

5. Figure out your debt situation: If you’re lucky, you won’t have a lot (or any) debt. For most of us there is some out there, and that isn’t necessarily a bad thing. List out every debt you have (student loan, mortgage, credit card, car payment, etc.), the balance, and the interest rate.

On a spreadsheet (see #4) rank them in order of interest rate. As a general rule I use a cutoff of about 6%. If your interest rate is above that pay those off right away, starting with the highest interest rate debt first. If your interest rate is below that, that might be okay to keep that debt and just make the normal monthly payments.

If you have any debt (especially credit card debt) at any rate higher than 10%, that’s a “debt emergency”. Really look at every purchase you make—if it’s not critical to your survival (food, shelter) then pass that up until your debt is paid off. The only exception to this is #1—funding your 401k.

You can get creative with your debt by consolidating high interest rate cards onto a lower rate card or one that offers a low teaser rate. That could save you a ton of money, and you should probably look into that, but ultimately, you’ll need to pay that sucker off. So just hitting the grindstone of paying off your credit cards is a must.

4. Make a budget on a spreadsheet: Take a spreadsheet and put a quick budget together that includes your income, your expenses, and the difference between those two. This can be simple at first (and it should be simple at first). Over time, you’ll add more and more sheets to the spreadsheet for things like your mortgage, investments, kids’ education, and other things.

But at the beginning, you need to get a sense of where your money is going. The budget will give you an aspirational view of this. After your budget is done, you can track your spending with a website like mint.com. This two-step process lets you figure where you want to spend your money, and then also look at where you actually spend it.

Of course, this is an iterative process, and as you close a month and look at your expenses, you can see if you’re spending more than what you budgeted. This isn’t a time to beat yourself up (being too hard on yourself is a sure way to stop looking at your finances closely, and that’s a REALLY bad thing), but a time to ask yourself why you spent more and if it was worth it.

As an aside, using a spreadsheet is a really good skill in general. I was really good at spreadsheets and it’s hard to overstate the incredible impact it had on my career, as well as the incredible wealth those skills gave me and my family. And really, my experience with spreadsheets started in college when I was creating a financial budget.

3. Educate yourself on investing: At a young age, educate yourself on investing. Obviously, this blog is the universally acknowledged best place to learn about investing, but I have heard rumors there are others.

www.mrmoneymustache.com is a great website that looks at personal spending and his early posts had a tremendous impact on my outlook. A Random Walk Down Wall Street is a book on investing that really defined my investing strategy; I read that as a 19-year-old and still think about its insights today.

There are a lot of websites written by millennials about spending and personal finance that might resonate even more. A few are: millennialmoneyman.com, moneypeach.com, and brokemillennial.com. Most are about reducing spending and budgets and that sort of thing, but there are some on the nitty gritty of making investing choices. You’ll want perspectives on both.

The whole point is that you need to know what you are doing here. Spending 20 hours early in your life to figure out basics like asset allocation, tax avoidance, and fee minimization as well as a general attitude towards saving early can easily lead to hundreds of thousands or millions of dollars. That comes to about $50,000 per hour—not bad.

2. Start an IRA with $1,000: This is as much about the experience gained as it is about actually investing your money. Vanguard lets you start an IRA with $1,000 as the minimum amount.

You’ll navigate through their website, figure out how to make choices (like Roth or Traditional IRA—go traditional). You’ll pick your investments, and then you’ll have something to look at every once in a while to see how it’s doing.

So many people are just at a total loss when it comes to setting up accounts for their investments. That becomes a real problem once you hit 30 or 40 and you’re starting to get behind the 8-ball; you know you need to do something but are kind of clueless on where to start. Doing it now lets you get your toes wet in this world and makes the next accounts you need to set up (529, 401k, brokerage, etc.) all the less daunting.

1. Get the company match on your 401k: #2 was more for experience than for investment. Here is where you should start walking down the path for investments. At a minimum, contribute the match and take the free money.

This is so important for a couple reasons. First, you’re getting that free money. Second, you’re making your first “asset allocation” decision. When it comes time to pick which fund to invest in, unless you have very unique circumstances for an early-20s person, I would definitely go with a 100% equity index fund.

Third, your 401k is a really powerful tool. If you had no other investing tool, you could still grow a 401k to well over a $1 million during your working career. That is enough to fully fund your retirement.

BONUS—Stay poor: Too many young adults make a huge mistake of trying to mimic the lifestyle their parents provided, once they (the young adults) get out of school. That first paycheck of $2,000 is going to seem like a ton of money (and it is). It’s really tempting to decide to buy a new car or go on a kickin’ vacation or upgrade the furniture. Resist the urge.

Your parents took 25 or more years of working (with pay increases and investment returns) to provide the house and cars and vacations you enjoyed your senior year of high school. It’s not realistic to think you can have stuff at that level of niceness so early.

A car is a really good example. In general, automobiles are horrible investments. To the degree you have a car that can get you from point A to point B, keep it. A new car will be nice and cool and make your friends gawk, but it’s a horrible use of money. A couple hundred dollars a month for a car, plus insurance, and maybe $50 for a gym membership, $50 for cable, and $80 for four dinners at a restaurant—those numbers add up. Those alone could fund your savings in the early years.

Your early 20s are a time when it’s still okay not to have the best and nicest of everything. If you can embrace that, even when you do have the money, and put that extra money to work in investments you’ll build a very strong financial foundation that will afford you many more opportunities are you reach your 30s and 40s (remember, I did that and I retired at 36).

The US has a complex tax code. That means people are always looking for ways (hopefully legal) to reduce the amount they owe in taxes.

Tax loss harvesting is one way you can do just that. The option isn’t always available; you need to have investment losses which means you can only do it in years the market is down. Through November, US stocks were slightly down for the year while International stocks were down significantly. That created the situation where you might be able to do some harvesting.

There are some intricacies with the tax law here. Remember that I am not an expert, so if you do this, you may want to consult a tax professional.

What it is

We all know that when you make money in the stock market (sell stock for more than what you bought it for), you are taxed on that gain. That’s called a capital gain. The opposite is true for losses; when you have a loss (sell for less than what you bought it for), you can reduce your taxes. Wait for it . . . those are called capital losses.

Tax loss harvesting is selling some of your investments at a loss, and then using that capital loss to reduce what you owe to the government in taxes.

How to do it

The strategy is pretty simple. When markets are down you can sell some of your investments at a loss.

Then at the end of the year, you can claim that loss on your taxes. The loss will offset any stock gains you have (either capital gains or distributions/dividends). If you still have losses after those have been offset, you can reduce your taxable income by up to $3000. That last part is a pretty sweet deal, especially if you are in a higher tax bracket.

Tactically, you just go to the website with your accounts (www.vanguard.com or www.fidelity.com or where ever) and sell those investments which have a loss. The in April when you pay your taxes, you get the tax forms from your brokerage house, and put those in your tax forms. Easy.

Why it’s important

The major benefit is that you are reducing your tax bill . . . now. Notice how I said that. Ultimately, you’re doing all this to lower your tax bill now and have it increase at some point in the future. Make no mistake, at some point or another you will need to pay taxes on your gains, it’s just a matter of when.

Obviously, having more money now instead of giving it to the government is a good thing, even if you’ll have to give it up later. Beyond that, there is the potential to create real dollar savings instead of just delaying when you pay taxes.

Capital gains and qualified dividends are taxed at three different rates, depending on your income.

Income (for married couple)

Tax rate

$0 to $77k

0%

$77k to $600k

15%

$600k+

20%

If you can use tax loss harvesting to influence when you pay taxes on those capital gains, there is the potential to recognize them when you’re in a lower tax bracket.

For Foxy Lady and me, we are in that middle tax bracket, so we would pay 15% on any capital gains and qualified dividends. However, if we did harvesting now and then recognized those gains in a year when our income was lower (below that $77k threshold), it’s possible that we could lower our rate from 15% to 0%. That’s real savings.

Doesn’t that defeat the purpose of investing

When you tax loss harvest you’re selling your investments, obviously. That could lead to another problem that you’re pulling your money out of the market, and you’re pulling your money out when stocks are down which seems like the absolute worst time. Likely you don’t want to do that; certainly, all other things being equal, pulling your money out at a loss isn’t what we’re going for with investing.

Actually, you can just trade your investments. So you can sell mutual fund ABC at a loss and simultaneously use those proceeds to buy mutual fund XYZ. You get the benefit of the tax loss but stay in the market.

The IRS understands this and has rules. You can’t sell ABC, recognize the loss, and then immediately buy back ABC. You have to wait 30 days to do that round trip.

However, you can buy something similar. The IRS says it can’t be too similar, but they don’t strictly define that so it’s a gray area. I personally, think it’s fair game to sell a broad mutual fund and buy another that is similar but still different (maybe a total international mutual fund gets sold and a total world mutual fund gets bought). You are still fully invested and largely have similar exposure, but you get that tax loss which is the whole point.

I don’t think this is something that is going to make you rich (like asset allocation or lowering fees—those strategies will make you rich). But it could net you a couple hundred or maybe even a couple thousand dollars. Who says “no” to that?