About two years ago we broadened our investment portfolio with this new-fangled things called peer-to-peer lending with Lending Club. This has turned out to be a pretty major disappointment for us, and we are in the process of exiting the investment (which isn’t a quick process—more on this in a second).

Basically, the idea of peer-to-peer lending is like match.com for lenders and borrowers. People who want to invest/lend money meet people who want to borrow money. Borrows can get money they need at much lower rates and much less hassle than if they got a loan from a bank. Lenders can earn interest at a much higher rate than they would get from a bank. Banks are cut out of the process and everyone wins, right?

How it works

There are people looking to borrow money for debt consolidation/payoff credit cards (that’s about 80% of the loans), help their small business, pay for home renovations, etc. Let’s say a given loan is for $10,000. A bunch of lenders like us each kick in $50 or so, so you’ll be in this loan with hundreds of other people. The person gets the money and then pays off the loan over 3-5 years.

Lending Club vets each loan and each applicant, and assigns a credit score. That credit score determines the interest rate which can range from 5-20%.

As a lender you can go through all the thousands of loan application and pick which ones you want to lend to. That’s fun at first, but quickly becomes a hassle, so you can just put it on auto-pilot and Lending Club will pick the loans for you. That’s what we did.

What happened to us

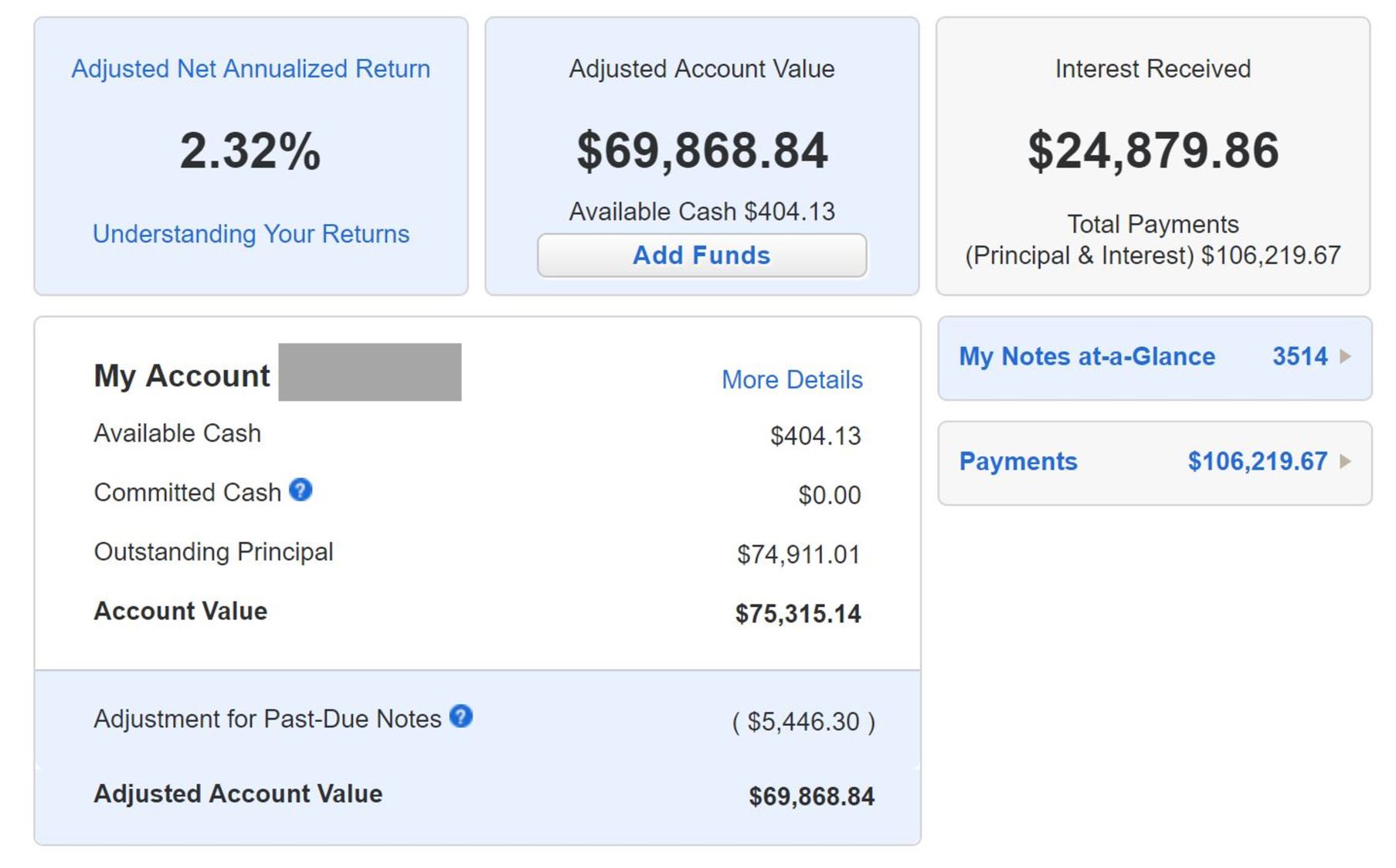

In mid-2015 we opened our account, starting with $3000. Of course, I watched the process like a hawk, from the loans I picked to when they started paying back. At first it went great (isn’t that line in pretty much every movie, before everything goes to hell?). We were getting paid back by all our loans, and our return was over 12%, which of course is amazing. That’s free money.

We put more money in over the next couple months, and then when we sold our California house we put a big chunk ($60,000) in. By that time, our account was worth about $100,000. Through mid-2016 things were going well. Our returns had inched down to about 10% (still spectacular), and I was congratulating myself on being a financial genius.

Towards the end of 2016 I started to see some of my loans default. Of course, this is to be expected. Some of the loans will go bad but those should be offset by the higher interest rate, and everything works out. Still, it was a disturbing trend.

After a few months, the bad loans kept coming and my return steadily dropped, until it settled at 2.5% which is where it’s at today. That’s crazy!!! Obviously, there’s a huge difference between a 10% investment and a 2.5% one.

In early 2017 I decided to pull the plug, and stopped reinvesting my money. Now, as the small loans (we have about 3000 out there) pay off, we take that money and put it back in our Vanguard account. Unfortunately, this isn’t a fast process so it will take us about 5 years to unwind everything. Oh well.

Why it works (or doesn’t)

On paper it sounds like one of those awesome ideas where the power of the internet changes an old business model for the better, and I think there’s a lot of truth in that. It brings borrowers and lenders together and cuts out the middlemen, and lowers the borrowing costs substantially.

The problem lies in their ability to ensure payments are made. Fundamentally, what is stopping borrowers from getting the money and then just going away and not paying? It may not happen a lot, but it doesn’t take a lot of these to really kill your return.

I have a bit of insight here because I was a large enough account that I would get a call about once per quarter from them “seeing how I was doing”. You can imagine the tone of these calls changed as my return dropped.

These loans are unsecured, so the only thing that makes borrows pay back is morality (I never want to count on that when it comes to money), the threat of negative marks on their credit rating, and the general badgering from Lending Club as it tries to collect. With traditional bank loans that are collateralized, the threat of repossessing something seems a lot stronger.

Not difficult to predict, there was a large portion of the borrowers who would take the money and then not pay it back. Some might be thieves who borrowed the money in a scam and never intended on paying back. Others certainly intended on doing it but things didn’t work out. Given the economy has been super strong the past couple years, this is especially troubling because it should be as good as it gets right now.

When someone stops paying Lending Club goes after them with phone calls, but those don’t seem really effective. Seriously, what are they going to do? Some delinquent borrows do starting paying back but most either never answer the phone, or they do and say/demand that Lending Club quit bothering them (there are actually notes lenders can see on all this activity).

I personally think that in our litigious environment today, lenders don’t have that much leverage. Also, to avoid claims of bias or discrimination, it’s probably not easy to turn down borrower applications. That leads to a perfect storm of crap that I think I got caught up in.

What is the lesson?

Investing is an interesting psychological experiment. The simple approach of buy-and-hold broad index mutual funds is almost certainly the best, yet it’s the most boring. When you’re doing that and things are going well, there’s that itch to see “what else you can do” and “what you can do better”.

That’s what happened to me, and most of the time that’s death. That’s what happened with us and our commodities investment, which has been a major loser. That was also the case with Lending Club, and we’ve had disappointing results (especially since stocks are up about 15% annually in the time we’ve invested in it).

So the lesson here is that it’s probably always better to stick with the boring but tried-and-true approach. History is on your side here. We have over 100 years of data on how stocks behave, in good times and bad. Peer-to-peer lending is fairly new so you don’t really know how it will play out. Maybe you’ll miss out on something that’s new but amazing (see: Bitcoin), but that leads to an interesting second point.

Many leaders—NFL head coaches, CEOs, politicians—say that success finding all the great things, but more avoiding the bad things. Stocks are similar. It’s a game rigged in your favor, but there are pitfalls along the way that are so tempting. That’s where I think I tripped up. Lending Club and commodities were sexy investments at the time, and it scratched that itch for me to be “doing something.” And it hurt me.

Of course, that doesn’t mean we never innovate. Peer-to-peer lending may turn into something big; digital currencies might turn into something big. They might be important parts of a financial portfolio, but I think now is way too early a time to be putting my money down on that bet. I know I’ll miss some big wins, but hopefully I’ll also avoid big losses and come out ahead.