I’m trying to build my audience, so if you like this post, please share it on social media using the buttons right above.

Holy Crap!!! That’s really the only appropriate response to the craziness of the stock market over the past few weeks. So over-the-top has been said craziness that I just couldn’t sit on the sidelines any more. I had to get my stocky back on.

Let’s dive in with what’s really going on, how crazy is all this really, and if you should be freaking out?

The numbers

Let’s try to remove emotion from the craziness of the stock market for the past few weeks and just look at the facts, the numbers.

On February 19, the stock market* peaked at 3386. The next two days it fell a bit, but then on Monday, February 24, it slipped over 3% and the freefall began. Since then it has plummeted to 2711, a 20% decrease. That’s a crazy fall but let’s put that in perspective.

First, before all this began, the stock market was up a bit less than 5% for the year (not bad for two months). So really we’re just down about 16% year-to-date. That’s certainly not good, but being down 16% feels better than being down 20%.

Second, despite all of this, we are up about 9% from where we were at the beginning of 2019. Going back five years, and the market is up about 32%.

You get my point. This is definitely bad, but I think one of the things that makes it so bad is that the pain has been so focused. Who knows what next week will bring (I am writing this Sunday night after the cubs finally went to sleep). Maybe the market is taking another dump on Monday morning as you read this. But those historical numbers seem decent. If someone told you at the beginning of 2019 that stocks would be up almost 10% over the next 15 months, I think you’d probably take it.

Historic context

The past three weeks (17 trading days) have been bad, even by historical standards. But how bad really?

In the past 17 days we are down 20%. Since 1928, there have been 15 other periods that bad or worse. Over 90 years, this has been worse 15 times. That doesn’t seem all that bad, actually.

Of course, that doesn’t mean this happens every six years or so. It’s much more lumpy. As you would probably guess, most of those 15 periods come from the Great Depression, eight of them in fact. That accounts for half of those instances. Needless to say, the Great Depression was a colossal economic calamity the likes of which we’ve never seen since. This is not going to be another Great Depression. Not anything remotely close to that.

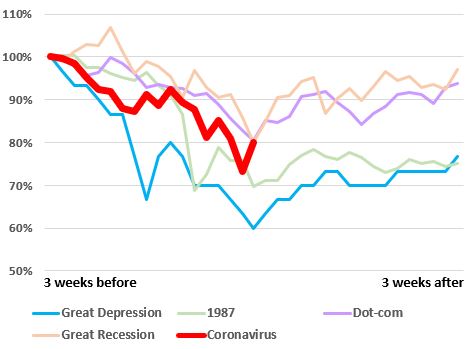

The others are a smattering of instances around World War II (1937, 1938, 1940, 1946), the biggest single day fall in the stock market’s history (1987), the dot-com bubble (2002), and the Great Recession (2008, 2009).

This time seems a bit middle of the road compared to those mega-examples. The graph shows the stock market in the three weeks before the you-know-what hit the fan and the three weeks after. What we are going through today is in the bright red line.

This gives me a bit of comfort. Coronavirus had a steeper fall than most, after three weeks (where we are today), it was as good or better than any of those examples. In the following three weeks thing improved in every case (for the Great Depression it got a bit better as you can see, but then the bottom really fell out).

Of course, it’s impossible to predict the stock market, but I tend to think things aren’t nearly as bad as the stock market’s performance would lead you to believe. Let’s say I’m 70% optimistic and 30% pessimistic.

The argument for stocks recovering quickly

If you compare what we’re going through to the dot-com bubble and the Great Recession, I think we’re in a lot better shape.

In each of those examples, there were fundamental and systematic problems with the stock market and the economy. In 2002 there was rampant accounting fraud (Enron, Worldcom, Qwest, etc.) that made it impossible to invest based on trustworthy information, the lifeblood of the stock market. In 2009 the banking system was collapsing, threating to grind the wheels of commerce in the US to a halt.

Coronavirus just doesn’t seem all that bad in comparison. Those were deep, dark issues that took a long time to unwind and correct. That doesn’t seem to be the case here. In the next few weeks the number of new cases will peak. Social distancing, warmer summer weather, and the miracles cooked up by the pharmaceutical industry are going to fix this.

If you look at data from China (not a good idea since I don’t trust their data) and South Korea (I trust their data more), this doesn’t last very long. South Korea started getting cases on February 19, and the US started getting cases on March 2; so we’re about two weeks behind them. Their new infections peaked on March 3; if ours follow suit we should be peaking this week. Even if it takes us twice as long to peak, that’s only another few weeks. That doesn’t seem all that bad.

Things are starting to turn for Koreans positively in other ways too. People are starting to recover to the point where the total number of people infected is flat—every day just as many people are considered fully recovered as there are new cases. Also, their death rate is falling precipitously.

Even if it takes us twice as long to peak and then flatten as it did in South Korea, that’s only another few weeks. That doesn’t seem all that bad. It’s definitely better than the Armageddon scenario that seemed to be priced into the market right now.

Going into this, the economy, especially the US economy, was quite strong and there’s no real reason to think that will change. Banks aren’t going to start much stricter lending regulations as was the case in 2009. You don’t have entire industries that we thought were very profitable and now we know are unprofitable as was the case in 2002.

Once we get the all-clear, there’s no real reason to think things won’t go back to normal, or maybe even better than normal as we work off some of that pent-up demand.

The argument for stocks still facing trouble

As optimistic as things look for South Korea, they look that bleak for Italy. Italy got their first cases a few days after South Korea, but they have yet to peak. Everything is on total lockdown and there isn’t an end in sight.

If we end up looking more like Italy than South Korea, that’s bad, obviously. Reasonable people can debate which is the better analog.

As it stands, in the US, the hits keep coming. Major components of industry are shutting down (mostly sports, travel, tourism, and conventions). Very honestly, this became real for me last Wednesday. That’s when the NCAA announced fans wouldn’t attend the basketball tournament (I had tickets) and the NBA cancelled the season (the NBA playoffs are my Christmas).

On Friday we started an international travel ban. Yesterday our state joined many others in cancelling schools for kids.

There’s an obvious human cost to all that, but there’s also an economic cost, one that will never be recovered. You can’t get the revenue for those tickets back, enjoy those cancelled cruises, fly on those cancelled flights. That’s all gone. At a minimum that’s probably 3-5% of the value of the stock market.

And that’s if things go right. There’s a lot of reason to believe that other industries might need to shut down. There’s also a lot of reason to believe that this might take months rather than weeks. As those things happen, it will get worse for stocks.

So there you go. That’s my take on all this crazy coronavirus mayhem. Sadly, this has given a lot of material for future posts, so you should expect another post from me on Wednesday. Ha, ha!!! That’s not sad, that’s great news.

*Unless otherwise stated, I’ll be using the S&P 500 when I refer to “the market”. For stock data before 1950, when the S&P 500 began, I am using a “proxy” of the S&P 500 that Yahoo!Finance has created going back to 1928.